Stock Research #9: Aritzia

Date of Research: 8/23/24

8/23/24 Close: $45.58 CAD

9/26/25 Close: $86.42 CAD

Research Sheet Aritzia

Company Description

Aritzia Inc., together with its subsidiaries, designs, develops, and sells apparels and accessories for women in the United States and Canada. Their product mix is wide, with a focus on high quality clothing at a premium price point.

Market Cap $5b CAD or ~$3.7b USD

Debt

Aritzia has a 2.99x leverage ratio, with $714m CAD net debt on the balance sheet, which is high, but in line with expectations of a growing company, with many stores opening in the near term.

Investment Thesis

From a fundamental standpoint, Aritzia is a growing brand with established business in Canada, but has recently expanded to the US and experienced strong growth in store count and revenues. Further revenue growth will be driven by store expansion in the US, and the company has experienced strong economics in this area, with store payback time beating internal estimates. The company expects strong margin expansion in their 2025 fiscal year, and according to CapIQ estimates, EBITDA is expected to expand from ~$220m CAD to ~540m CAD.

In terms of valuation, I expect that Aritzia will continue to trade at a premium due to its near term growth potential, as well as strong operating figures. Weakening consumer sentiment and overabundance of supply similar to what the company experienced in 2023 would likely result in a de-rating from this point. With the macro environment seeming extremely volatile, this seems like a bet on the soft landing working out, and a strong company in the consumer discretionary industry.

Main Drivers

Store Growth and Customer Acquisition

On pace for total square footage growth of 50% in the US in 2024 – driven by 12 new and repositioned stores in the next 5 months

Opening of new Boca Raton location beat internal sales projections by 35% and is tracking to payback in 10 months vs. the forecasted 12-18 months

60% of the Boca Raton customers were new to Aritzia, illustrating strong potential for growth through customer acquisition in untapped US markets – figure is consistent with recent store openings, Sacramento was around 50% new customers as well

Have identified 150+ locations for new store openings and plan to open 8-10 stores annually

Margin Expansion

Management expects margins to expand due to lower warehousing costs, and stronger pricing with lower markdowns

Strong Demand from Core Customers and Seasonality of Revenues

Aritzia’s annual warehouse sale brings out their core customer base, and is a major event that draws in massive lines similar to those seen at amusement parks

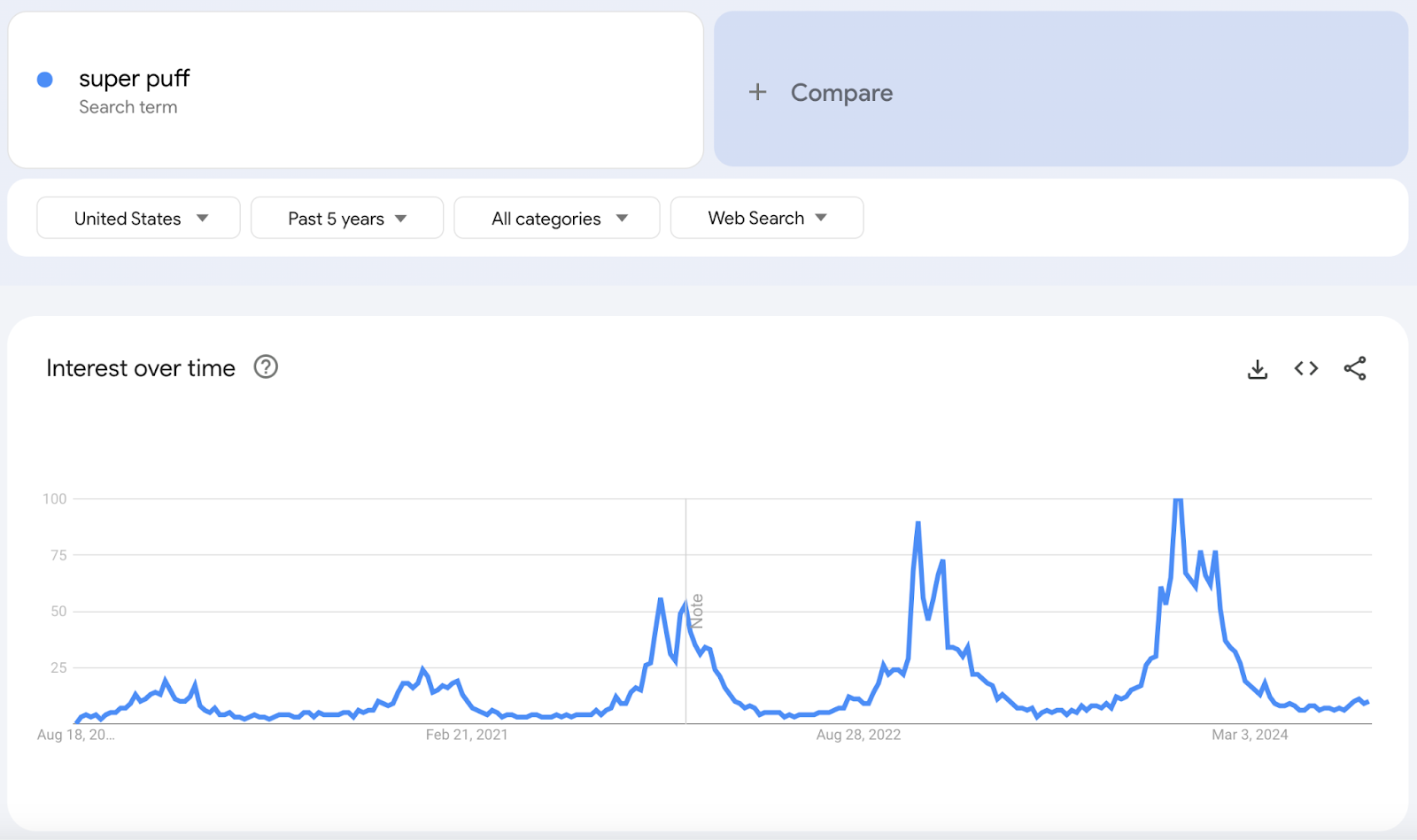

Seasonality of revenues could drive strong Q3 and Q4 calendar year performance; the Super Puff jacket is a highly sought after item, similar to Canada Goose, but at a lower price point ($200-$500)

On TikTok, the hashtag #Superpuff currently has 89.7 million views (Glossy, Dec. 8, 2023)

Created the super puff 7 years ago – has grown in popularity each year since

Catalysts / Re-Rating Potential

Margin expansion (EBITDA margin increasing from ~10% in 2024 to a forecasted 20% in 2025)

Good figures on store openings and customer acquisition in Q2 2025 earnings report in mid October

Costs

SG&A expenses increased by 14.9% to $176.3 million, compared to $153.5 million in Q1 2024. SG&A expenses were 35.4% of net revenue, compared to 33.2% in Q1 2024. The increase in SG&A expenses was driven by investments in digital marketing to protect and propel the Aritzia brand, infrastructure projects, and technology initiatives to support the Company’s growth

Valuation

Aritzia trades at a discount to its historical valuations, (22.8x NTM EPS vs. 30x NTM EPS) but at a premium to its comps set. (22.8x vs. 10.7x NTM EPS) I believe this premium is deserved due to Aritzia’s near term growth potential and strong pricing power they have illustrated in a tough macroeconomic environment

ESG

“100% of the energy fuelling our Boutiques, Support Offices, and Distribution Centres comes from renewable sources1 achieved through purchased Renewable Energy Credits (RECs)”

Aritzia ESG Report FY24

Positives

Strong YoY revenue growth of 13% in the US, their primary growth area

CFO projects FCF generation to increase in the back half of fiscal year 2025, as capital expenditures normalizes – in Q&A transcript, CFO mentioned that the company will prioritize the share repurchase program once this FCF is realized

CFO projects gross profit margin expansion of 450 bps in the 2nd quarter of fiscal year 2025, driven by pricing (150bps) , lower warehousing costs (125bps), and lower markdowns (100bps)

Q1 2025’s 510bps gross profit margin expansion was driven by leverage on fixed costs as well as lower markdowns resulting in fuller pricing of products

Stock is up 62% YTD after strong earnings results for Q1 2025

Negatives

Comparable sales growth of 2% is low; but not too concerning if new store openings can continue

One driver of an increasing gross profit margin was ‘IMU improvements’ which just means higher initial markups; it will be interesting to see how the consumer responds to this and if volumes can stay high with prices increasing as this is a discretionary business

Company experienced difficulties in 2023, stock fell 40% as inventory increased and consumer weakness led to weaker performance, stock has rebounded a lot since then, indicating investor confidence in management

Upside Risks

Soft landing in play after a potential rate cut in September, could lead to stronger consumer spending than at present

Downside Risks

Highly sensitive to consumer sentiment and lower consumer spending would have drastic effects on luxury clothing brands like Aritzia

Sources

https://x.com/NewcomerInvest/status/1701008756707111205

Images