Stock Research #8: Greggs PLC

Date of Research: 8/15/24

8/15/24: £3158.00

9/26/25: £1596.00

Total Return: (49.48%)

CAGR: (46.52%)

Research Sheet Greggs Plc

Company Description

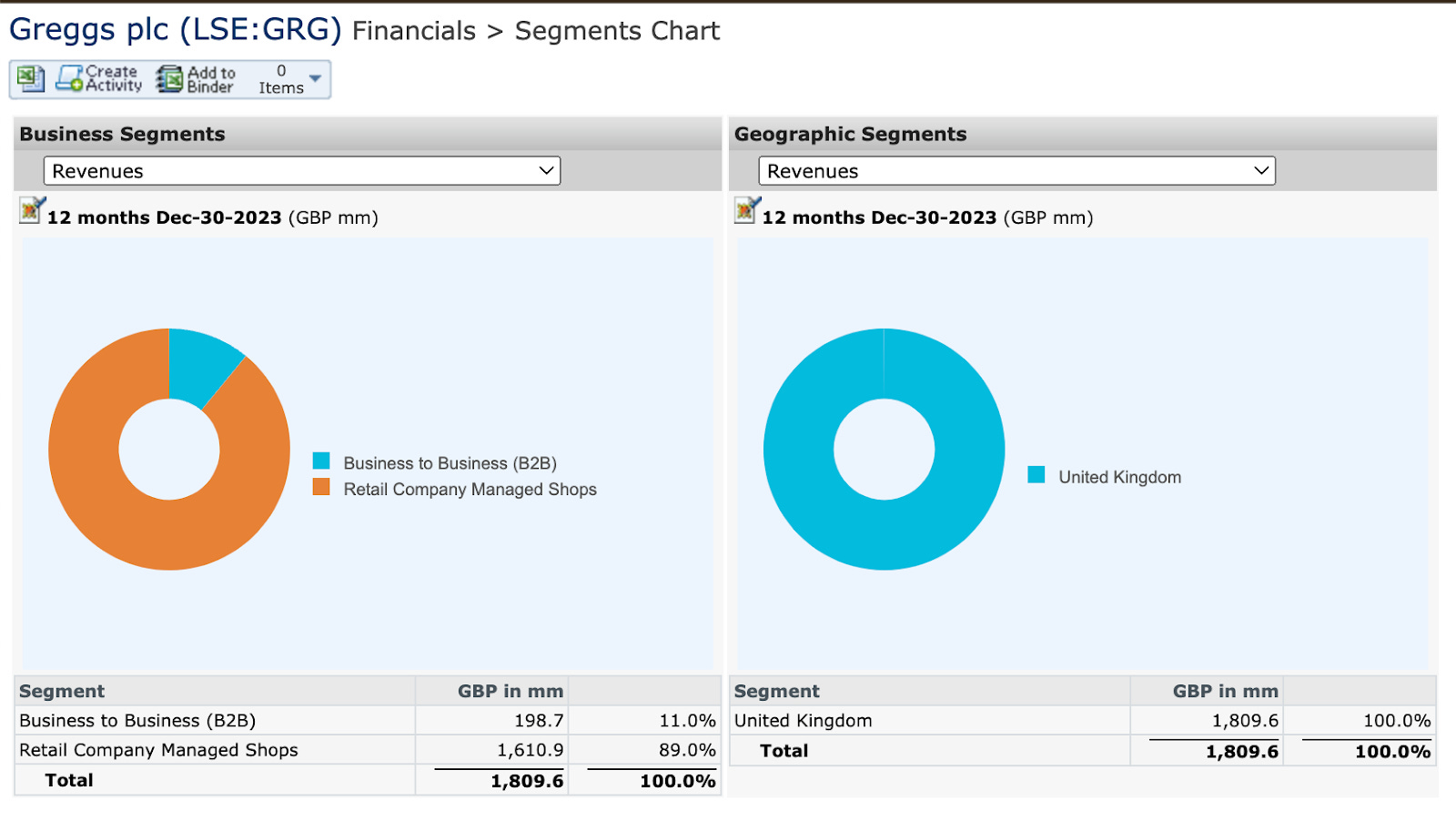

Greggs Plc is a food on the go retailer, selling baked goods, sandwiches, and beverages. They sell products to franchisees, and wholesale their goods as well. Greggs’ largest segment is selling through their company managed shops, composing 89% or £1.6b of their £1.8b of sales in 2023. The other £200m comes from their B2B business segment, which includes wholesaling and franchise partners. The business-to-business segment is their fastest growing, with 24% YoY growth from 1H23 to 1H24.

Debt

Greggs Plc has an attractive balance sheet with only £238.2m in net debt, so a 0.7x Net Debt/EBITDA ratio compared to its comp sets average of 3.2x.

Investment Thesis

The investment thesis in Greggs is pretty clear: you’re buying a steadily growing company with strong vertical integration, (2500+ shops, and 12 manufacturing/distribution centers) improving margins, (through strong pricing and cost inflation slowing) and a long term growth runway to 3500 shops in FY 26/27. Along with these factors, almost half of Greggs shops are staying open later (7pm vs 4pm previously) to help serve customers commuting back from work. While there isn’t one clear driver or positive change at hand, these factors, along with an improving UK-economy backdrop could drive the stock further.

The valuation thesis is that Greggs will continue to trade at a premium relative to its peers (23.3x LTM PE vs. 16x peer average) and continued revenue growth towards the £2.4b FY26 target will drive strong stock returns. Catalysts that could drive the stock towards an even higher premium would be increased dividend payouts, further rate cuts by the Bank of England, as well as improved margins that could be gained through the investments in their supply chain. Achieving this 2026 target, with similar profitability to now as well as similar valuation, would result in a 39% return from this point, excluding dividend payouts.

Main Drivers

Store Growth Program

51 net new shops in first half of 2024, on track for 140-160 new shops by EOY, Greggs is integrating itself into the daily lives of its customers, and providing consistent quality in many places, and at all times.

Company has stockpiled cash and plans to make large capital expenditures in 2024, focused on expanding their supply chain and increasing capacity to support ~3,500 shops (currently 2,524 so a roughly 40% increase in shops by 2026/2027)

Company projects to spend £143m in capex on the supply chain, ~50% of all capex spend in 2024. The company is focused on increasing capacity on current factories through renovations, they expect to add 300 shops worth of capacity to their Birmingham and Amesbury distribution centers. Additionally, they are projecting to finish construction of two new facilities in Derby and Kettering by 2026/2027, providing logistics capacity for an additional 700 shops.

Digital Sales Channels and Delivery Services

Greggs is expanding their offering, and currently has 1400+ stores that offer delivery services after 6pm. Greggs has “empowered our teams to ‘Fix it Now’, enabling them to substitute items for customers, instead of rejecting a delivery order.” In the long term, this could have massive effects on total volumes as typical restaurants don’t substitute food items. The company has also found that deliveries help serve, “multiple customers in one order with higher-than-average basket size.” Electronic point of sale software is being rolled out to Greggs locations, and could help increase labor efficiency and reduce costs.

Catalysts / Re-Rating Potential

Further dovish sentiment from the Bank of England (recently lowered rates from 5.25% to 5.0%)

Improved margins (Greggs is forecasted for a 3% increase in EBITDA margin from 2023 to 2024)

Continued dividend increases as margins improve

Costs

Greggs is benefiting from unexpected deflation in food and packaging, which allowed them to increase their profit before tax by 16% and their dividend by 19% to 19p/share.

Greggs has very strong gross margins compared to peers (61% gross margin compared to peer average of 36.2%) and their EBITDA margins are slightly higher. (13.4% vs 12.4%)

Valuation

Edison, an equity research firm recently increased the valuation slightly, claiming:

“A reduction in our estimated weighted average cost of capital (WACC) due mainly to a lower UK market risk premium to 4.8% from 5.5% (source: Damodaran) as well as modest changes to our estimates and updating for the financial position have led to our DCF-based valuation increasing to £31.90/share from £30.20 previously. The share price has performed well year-to-date, leaving the valuation at a deserved premium to its UK peers given premium revenue growth and profitability”

ESG

Prevent food waste by partnering with a food app “Too Good To Go” where customers get food that is expiring soon for ~40% of the typical costs, helps the firm recover some costs while lowering food waste

Greggs donates food that will go to waste to local charities

Goal to be completely Net Zero by 2040

Positives

Stable core business with a long term growth runway, per Edison Research, “forecast Greggs will continue to generate strong growth over the next three years, with CAGRs for revenue and operating profit for FY 24–26 of 11% and 10%, respectively. More than half of the forecast revenue growth is from new store openings, which should have a high level of visibility.”

They have recently experimented with their product mix, offering over ice cold drinks, as well as pizza and healthier on the go options like pesto chicken flatbreads. Greggs is committed to serving healthier options, with a minimum 30% of their products being healthier, a value proposition for health-conscious consumers

“In the 12 months to June 2023, the number of UK consumers who ate in fast food outlets increased to 45%”(Foodservice Report) – Consumer preferences are shifting towards fast food, and oftentimes that means sacrificing for unhealthy options, but Greggs is responding to that gap in the market by offering healthier options at a fast food price point and availability.

2026 target of £2.4b in sales, which would be a 26% increase from the LTM sales in June of 2024

Greggs is extending their operating hours; they have 1200 shops open until at least 7pm, and evening sales is their fastest growing customer segment, with their market share expanding from 1.2% to 1.6%

34 shops are now 24-hour drive thrus, and this store type is rapidly gaining popularity with shift workers

Click and Collect (C&C) sales channel offers customers another way to purchase – as our world becomes more digital, quick grab and go sales are increasingly common especially within the fast food industry (ex: Starbucks, McDonalds, etc.)

Strong moat in an industry with a high barrier to entry, recreating their supply chain, brand loyalty, and pricing power would be very difficult to do.

Strong historical ROE, 22.56% 5-yr average, with the last 3 years above 27%

Negatives

No clear “positive change” – more a story of multiple smaller changes that could make for outsized returns in the aggregate

UK’s National Living Wage could pressure margins, personnel cost inflation is a concern for management

Upside Risks

Input cost inflation decelerating, helping to improve margins – if this trend continues the margins will be even stronger, helping drive stock price

“Unlike many consumer-facing companies, high selling price inflation was accompanied by volume growth, leading to good market share gains”(Edison Research) – in this sense, inflation could be an upside risk in that Greggs has strong pricing power with the consumer

Downside Risks

Input cost inflation ramping back up; pressuring margins

Edison Research claims, “Following the UK’s exit from the EU, there remains potential for changes to regulations and supply chain disruption, including delays to the import of goods.”

Execution risk with a more rapid store expansion program than the company’s history could negatively impact the quality of new stores

Sources

Edison Research

Annual and Quarterly Reports

Images