Stock Research #7: Navios Maritime Research

Date of Research: 8/8/24

8/8/24 Close: $44.52

9/26/25 Close: $47.76

+ $0.25 of dividends issued

Total Return: 7.84%

CAGR: 6.75%

Navios Maritime Research Sheet

Company Description

Navios Maritime is a shipping conglomerate with a market capitalization of $1.3 billion USD. They are headquartered in Monaco, and have had a historically complex corporate structure that has since been significantly simplified. The current firm used to be five separate corporate entities, with complicated fee structures between some of the companies. As it stands currently, the controlling shareholder, Angeliki Frangou owns 16.75% of the company, and Navios Maritime is the only public Navios firm, so the complex corporate structure has been simplified, and the main shareholder/operator of the business has aligned interests with shareholders. Navios operates within three main shipping segments: dry bulk, containers, and tankers. Their exposure to each segment in terms of vessel value is Dry bulk (45%), Container ships (20%), and Tankers. (35%)

Debt

Net Debt / EBITDA or leverage ratio stands at 2.94x, so relatively high, but that comes with the shipping industry, and they plan to pay down large portions of the debt after the newbuild projects.

Investment Thesis

Fundamental Investment Story:

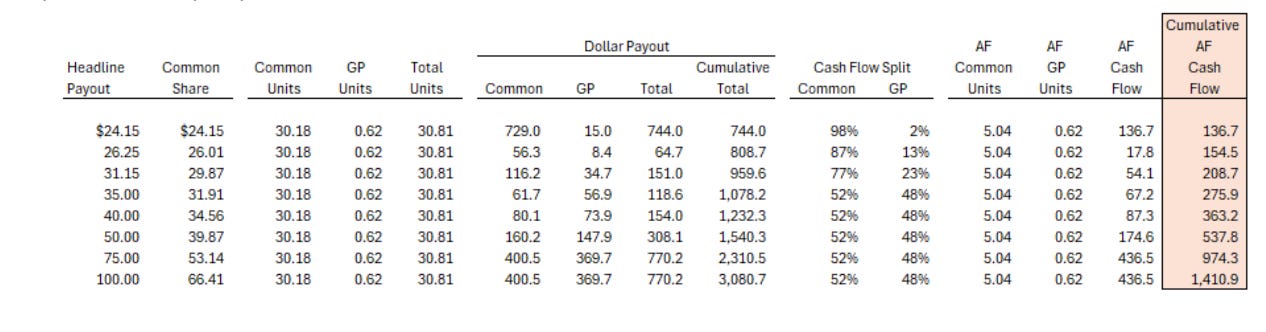

Navios Maritime is a diversified shipping conglomerate with dry bulk vessels, container ships, and tankers, and had previously been an amalgamation of 5 different corporate entities, now clearly merged into one firm. Navios is currently valued amongst the lowest of its peers largely due to low cash dividends to shareholders compared to the industry. (0.5% vs. peer average 5.1%) While Navios is rated amongst the lowest in terms of valuations, it experiences above average operating performance compared to the peers, namely Navios had a 48.3% EBITDA margin in 2023 compared to peer average of 35%. Across the board, Navios experiences in line or above average operating performance, and the only point of concern is the low level of cash dividends to shareholders compared with the industry average. In my opinion, this is likely to change for the positive in 2024 and beyond, with the controlling shareholder, Angeliki Frangou, taking Navios Holding Co. private in late 2023, along with taking possession of the incentive distribution rights that company held. These rights act as a general partner split, meaning that the larger the total cash distribution to shareholders, the more split that the IDRs receive. The IDRs only kick in at over $24/share, which would yield ~54% at current price levels. While this rapid increase seems unfeasible considering that current operating cash flow sits at ~$18 per share, and the prioritization of newbuilds and paying down debt has taken precedence over cash dividends, I think it is possible to see in the near term. Given that fundamentals are rising across the board, especially within dry bulk; which Navios is very exposed to, and the CEO is fully incentivized to increase cash distribution, I don’t think it’s out of the realm of possibility.

Valuation Investment Thesis:

The bet on Navios Maritime is particularly interesting because there are potentially multiple outs. The first opportunity is that management continues to make confusing capital allocation decisions, the multiple remains lower than industry average, yet fundamentals improve, along with revenue, and the stock goes up in line with revenue growth. Secondly, management could decide to increase cash dividends to industry average, and the multiple could re-rate by 50%, in line with peers, and along with revenue growth, the stock performs exceptionally well. Lastly, management can buy back shares, effectively paying 50 cents on the dollar for the ships they currently own due to the net current asset value spread, and the company could re-rate based on that. The way this bet could lose is that management continues to allocate capital poorly, and a recession hits and/or the high levels of demand fall, and fundamentals rapidly deteriorate.

Main Drivers

Capesize Day Rates – Day Rates are rapidly increasing with capesize vessels being priced at $27-28000 in Q4 of 2024. The Baltic Dry Index, a dry bulk shipping rate index is up 48% since this time last year.

“Adjusting for the higher earning potential of large vessels, as well as the long term contracted nature of its container and product tanker fleet, the true leverage to capesize day rates is likely 30-40% for NMM.”(Lake Cornelia Research Management Inc.)

The other segments (Containerships and Tankers) are heavily contracted out, providing downside protection – Contract cover for containers and tankers is ~90% for 2024

“We view these valuations as more stable because NMM has largely contracted out most of their ships. NMM has a $3.3 billion backlog of contracts (2023 revenue was ~$1.3 billion for context). Contract cover for containers and tankers is ~90% for 2024 and extends out for years. We view these other segments as providing downside protection and investment duration to the embedded capesize bet.” (Lake Cornelia Research Management Inc.)

The dry bulk bull thesis is supported by low supply growth in the sector

“The current orderbook stands at 8.1% of the dry bulk fleet. The supramax segment could grow the fastest, while the capesize orderbook remains small.” (Baltic and International Maritime Council)

Catalysts / Re-Rating Potential

Increase in cash distribution to shareholders, as management’s incentives are fully aligned with shareholders (incentive distribution rights in place)

Capesize rates pushing higher with increased demand and low supply growth

Removal of anti-takeover provisions

Costs

EBITDA margin is projected to increase steadily over the next two years to 54% in 2024 and 57% in 2025 from 48% in 2023.

Valuation

Trades at 50% discount to NCAV of $110/share, which assumes the newbuilds program generates zero shareholder value

Trades at 50% discount to peer average NTM PE ratio (3.09x vs. 6.14x) per CapIQ

ESG

Net Zero by 2050

Navios is one of the founding members of the global Maritime Emissions Reduction Centre in

collaboration with the Lloyd’s Register (LR) Maritime Decarbonisation Hub that will focus on

optimizing the efficiency of the existing global fleet.

Positives

27% NFY EBITDA growth projected; in line with the 25% average of the comps, indicating strong performance for shipping companies in the near term

Management is extremely inclined to increase cash distributions to shareholders, which at current price levels would be over 50% yield to shareholders

Disgruntled shareholders are writing to management – this sort of activism could spark management action to deliver value to shareholders via buybacks, dividends, or liquidation of some assets

Secondhand vessel prices are rising rapidly – could be a sign of scarcity within the sector (Tanker prices are up 98% since 2021, and Bulk Carrier prices are up 85%)

Diversified fleet value across 3 main segments – Dry bulk (45%), Container ships (20%), and Tankers (35%)

Seanergy Maritime, a peer, were just ranked as an outperform in an equity research report done on August 8th by Noble Capital Markets Independent Analysis, where they claimed “we think the fundamental backdrop remains favorable through 2024”

CEO is buying shares, picture of 13D below

Negatives

Historically has been amongst the lowest dividend yields in the industry, likely the cause of the low multiple assigned to the stock

Investor angst is rising, with many investors calling for liquidation of current assets to return value to shareholders

Anti-takeover provisions means it is unlikely that frustrated shareholders will have any ability to force management’s hand

Upside Risks

Tightened ship supply elevates freight rates – according to Clarksons, as of June 1, 2024, new shipbuilding orders for global crude oil tankers represent 7.7% of the existing shipping capacity, which is an increase since 2023, but still a historically low level; the supply for ships is very inelastic; if demand continues to increase, rates could go even higher. There is a similar story within the dry bulk segment, with the orderbook standing at only 8.1% of the current dry bulk fleet.

Huatei Research maintains an overweight rating on the shipping sector, and claims that:

Within container shipping: “Red Sea detours, seasonal peak, and port congestion are driving high market prosperity. Short term solutions to the Red Sea detour are unlikely”

“Tanker shipping: seasonal peaks will boost freight volumes, leading to a qoq increase in freight rates.”

“Dry bulk: seasonal demand will drive QoQ increases in freight rates.”

Downside Risks

Extremely sensitive to global macroeconomy, with recession risks rising, this stock really only makes sense if you believe the ‘soft landing’ is in play

JP Morgan has increased the odds of a recession by the end of 2024 to 35% with the weak jobs report that came out last week

Continued capital allocation to newbuilds and paying down debt instead of dividends or buybacks, stock could remain at current valuations due to investor fatigue

Navios Maritimes cash from investing was -$253m due to high capex spending on newbuilds and acquiring vessels

Navios Maritimes cash from financing was -$233m in 2023 due to debt repayments

Images

https://splash247.com/capesize-ffas-hitting-prolonged-highs-not-experienced-since-the-2000s/

https://docs.google.com/document/d/1L2jU_4bxosB5WbDzq20DhTvjMTlkoL4i_D9t3ekFPxE/edit

https://www.reuters.com/markets/us/jpmorgan-raises-odds-us-recession-by-year-end-35-2024-08-08/