Stock Research #4: TGS ASA

Date of Research: 7/12/24

7/12/24 Close: 127.50 NOK

9/26/25 Close: 76.15 NOK

Total Return: (40.27%)

CAGR: (36.32%)

TGS Research Sheet

Company Overview

Headquartered in Oslo, Norway

Market Cap: $2.4b

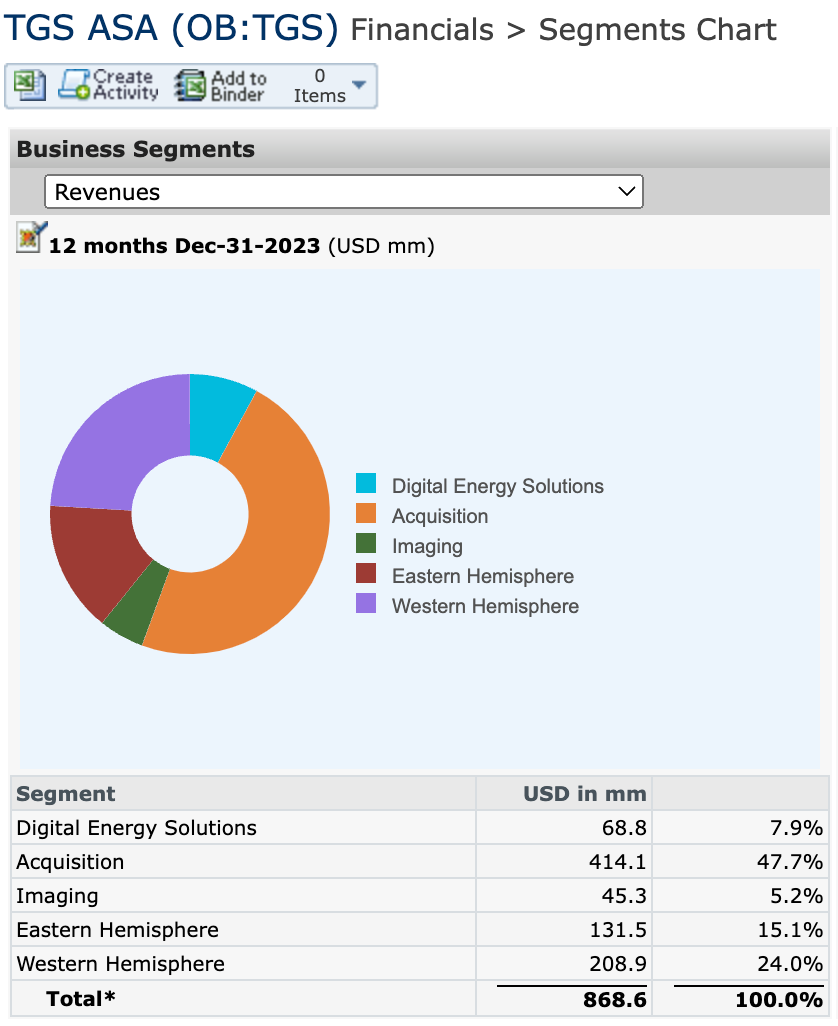

Business Overview:

Acquisition: Mostly composed of Magseis, the main function of the Acquisition business is acquiring ocean bottom node (OBN) data on behalf of customers, as well as sales of OBN-related equipment.

Digital Energy Solutions: includes energy transition products and services such as the offshore wind and Carbon Capture, Utilization, and Storage (CCUS)

Imaging: providing advanced seismic data processing and interpretation to support exploration and production activities

Their seismic data library is sold to multiple clients, so they refer to it as their “Multi-client library” throughout their financial statements

The Eastern and Western Hemisphere segments largely conduct the same business (Imaging, Data Acquisition, etc.) but are grouped separately in the financial statements

Financial Data:

Historical Growth:

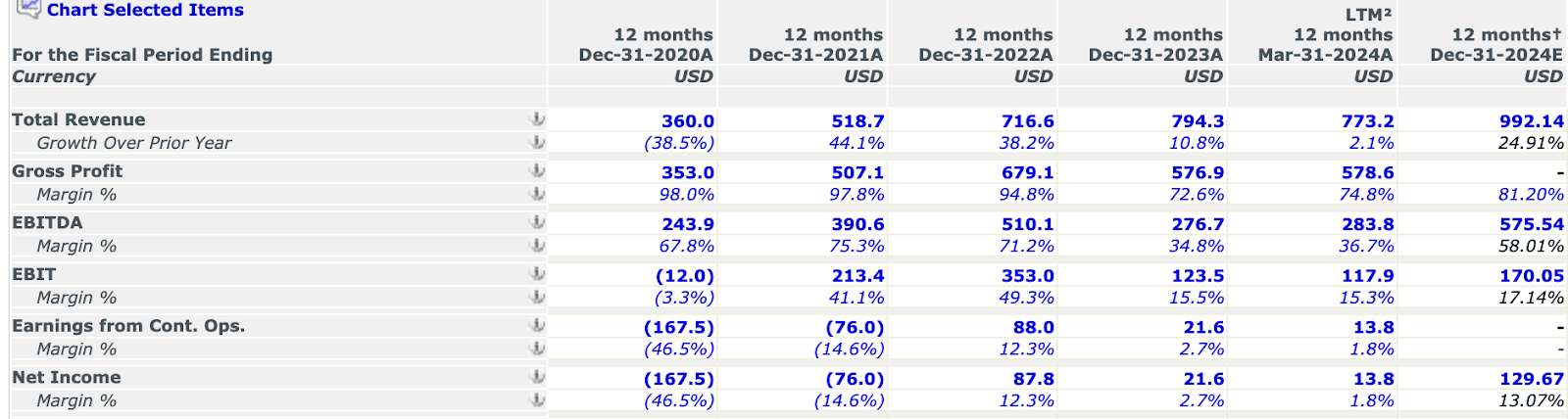

Topline revenue is decelerating; revenue grew 10.8% YoY in CY2023, following 38.2% and 44.1% YoY growth in CY2022 and CY2021, respectively

TGS has pursued an inorganic growth strategy via acquisition of Magseis and Polarcus data sets

Magseis’ revenue in CY2022 was $350m, approximately 44% of TGS’s CY2023 revenue of $794m

The Polarcus acquisition added 3D seismic surveys of 12.2k square kilometers off the shore of Australia in 2021

Recently finalized their merger with PGS (Petroleum Geo Services) on July 1st, who operated in the same industry of seismic data acquisition and imaging

Brought in $720.7m of revenue in 2023, but net income margins have been low or have resulted in net losses in previous years

Projected Growth:

NFY EBITDA growth is aggressively projected at 102%, driven by increased topline revenue as well as much stronger profitability (EBITDA of 58% compared to CY EBITDA margin of 36.7%)

TGS plans to invest $300-$350 million in multi-client data in 2024, with early sales projected to cover 85% of these costs, indicating strong demand for oil and gas exploration

The Digital Energy Solutions segment, which includes energy transition products and services, grew revenues by 62% in 2023 and is expected to continue expanding. This includes significant growth in offshore wind and Carbon Capture, Utilization, and Storage (CCUS) markets. This could be an opportunity for growth as the world shifts to more renewable energy.

Margins:

Margins have fluctuated heavily in recent years, likely due to macroeconomic conditions affecting the overall industry and oil demand.

Net Income was depressed in 2023, which could be attributed to a large amount of amortization that increased from $33.6m in 2022 to $96.9m in 2023.

Debt:

Net debt just turned positive in Q1 of 2024 at $41.5m, but compared to a TTM EBITDA of $283.3m they an extremely low leverage ratio of 0.146

Investment Thesis

Fundamental Opportunity: With rising demand for oil exploration, TGS is well-positioned due to its extensive seismic data library and ability to expand it. This extensive and high-quality data allows TGS to sell seismic information at a premium compared to peers. However, given that much of TGS’s growth is inorganic and driven by industry-wide changes, it does seem to fit EGA’s criteria.

Valuation Opportunity: The company’s valuation has potential to re-rate among peers, but it is likely fairly valued given recent margin fluctuations and the significant margin expansion (23.21%) needed to meet EBITDA estimates. When looking at their financial statements and investor relations materials, there was no notable ‘positive change’ to indicate potential for margin improvements.

Catalysts / Re-rating potential

Effective integration of the PGS acquisition, potentially receiving some cost synergies from the acquisition

TGS cites “Consolidations on the client side, near-term focus on mature basins and substantial synergies” as the rationale for the acquisition

Main Drivers / Sensitivities

Much of the focus in oil and gas exploration is in mature and developed areas where pre existing infrastructure can offer developed companies an advantage against peers, and TGS is positioned to benefit from these areas

“As our clients focus on exploration in mature areas with established infrastructure, the quality of data processing and imaging is becoming increasingly important. I’m pleased to see further improvements in our imaging quality, demonstrated by 41% growth in proprietary revenues and a prequalification status among the majority of our largest multi-client customers” - Letter to Shareholders 2023

With the acquisition of Magseis in January 2023, who specializes in ocean bottom nodes (OBN) , TGS is well positioned for a return to exploration activity in that segment. The OBN market has nearly doubled since 2020

There’s been a sharp increase in oil and gas upstream capital spending:

“Oil and gas annual upstream capital expenditures rose by $63 billion year-on-year in 2023 and are expected to rise a further $26 billion in 2024, surpassing $600 billion for the first time in a decade. Upstream investment in 2024 is expected to be more than double 2020’s low of $300 billion and be well above 2015-2019 levels of ~$425 billion.” per the International Energy Forum

Valuation

Historical average PE ratio is 19.5x NTM earnings per share, but disregarding outlier periods, it is likely closer to 10-15x earnings per share, so in line with the current 10x earnings that it trades at.

Trading at a discount to its industry peers, 10x earnings per share compared to 15.85x, so there is upside potential to re-rate alongside its peers

Costs

A large cost in 2023 was their effective tax rate increasing to an outlier 58%, which they cite as being due to currency movements and valuation allowances. Per the annual report: “Tax expenses amounted to USD 30.2 million, corresponding to an effective tax rate of 58%. The main reasons for the high tax rate were currency movements and valuation allowances made for certain jurisdictions. “

$13.47m of the $30.2m or 44.6% was attributed to withholding taxes and overseas taxes

Little information was given about why the tax rate was so inflated in 2023, and the projected tax rate for 2024 is not mentioned

ESG

Made significant strides in improving sustainability in 2023, TGS ranked in the top 40 companies in the OBX ESG Index

“In offshore wind, TGS has been innovative in applying a proven business model from seismic to allow operators access to data by deploying the first-ever LiDAR buoy measurement campaigns to support offshore wind development in both U.S. and Norway”

Positives

Pre existing data used for oil and gas exploration can be repurposed for their carbon capture and storage segment of the business – with their large seismic data library this could expand their offerings to an additional customer segment with minimal additional investment

“Our global subsurface data library and experience in data management and marine operations, position us well for future growth in the markets for offshore wind, carbon capture, utilization and storage (CCUS)”

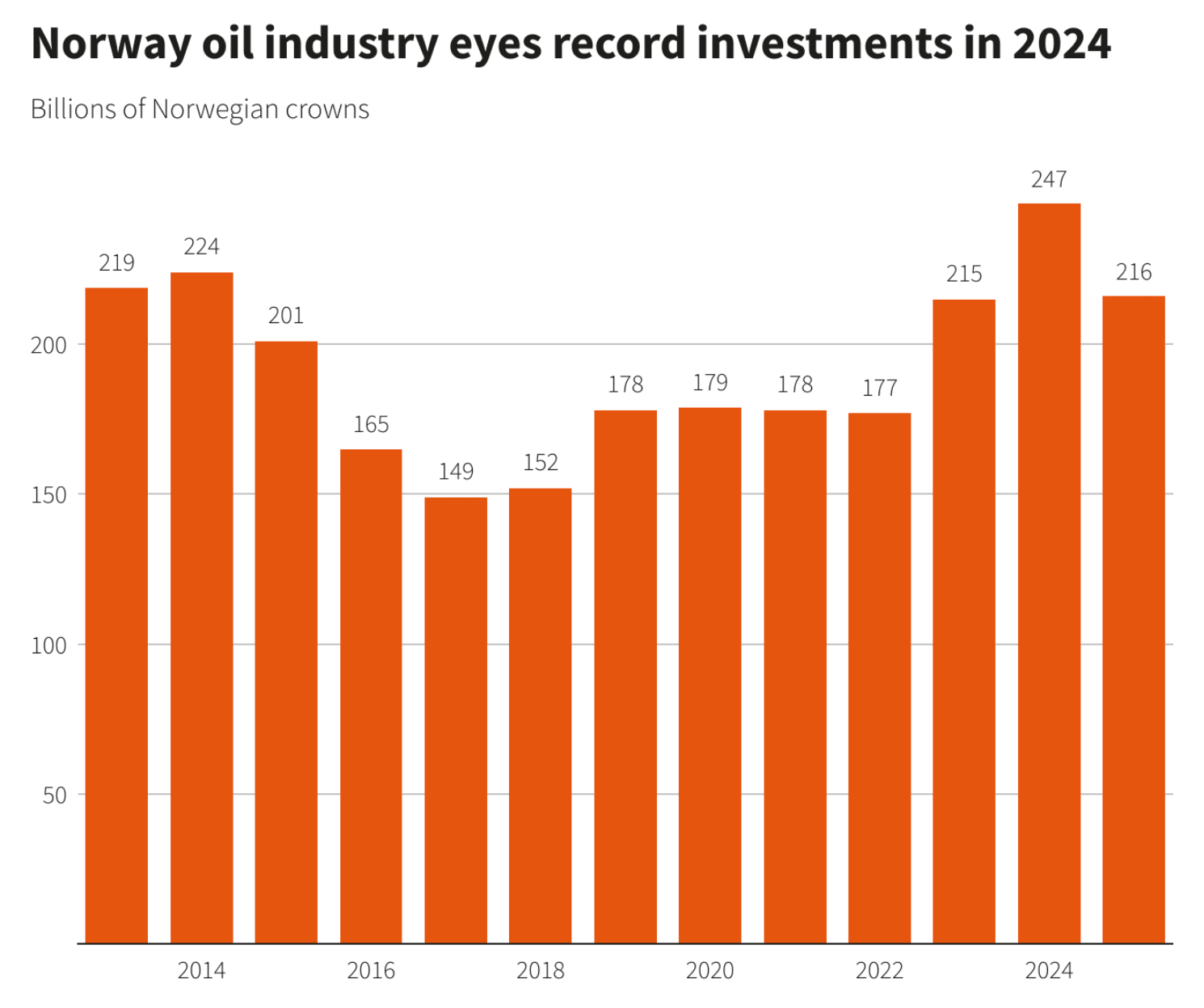

Investments in oil and gas, manufacturing, mining and electricity supply have grown 18.7% from Q2 2023 to Q2 2024 in Norway

Due to high non-cash expenses, they generated strong FCF margins of 12.4% in 2023, despite low net income margins.

$0.56 annual dividend per share, totaling $70m

Negatives

Tax Rate fluctuations, and the persistence of abnormally high effective tax rates

Inorganic growth being their main source of revenue growth in recent years – no positive change that I could see other than macroeconomic factors

In an on-cycle industry, the only cash being given back to shareholders is the dividend, no share buybacks

Upside Risks

The success or failure of strategic acquisitions, such as the merger with PGS ASA, depends on effective integration and realization of synergies

Downside Risks

TGS’s business is highly dependent on the oil and gas industry, which is sensitive to fluctuations in oil prices. Significant changes in oil prices can affect exploration budgets and demand for seismic data, for better or worse

Sources (Turn into PDFs)

https://www.offshore-technology.com/news/norway-oil-gas-investments/?cf-view

https://www.tgs.com/articles/growth-of-obn-in-gom