Stock Research #3: Austal

Date of Research 7/5/24

7/5/24 Close: $2.50 AUD

9/26/25 Close: $7.24 AUD

Total Return: 189.6%

CAGR: 138.8%

Austal Research Sheet

Company Overview

Austal is Australia’s largest defense exporter, and is one of only two foreign-owned prime contractors designing, constructing and sustaining ships for the US Navy. Austal delivers monohull, catamaran commercial platforms as well as defense vessel platforms. In 35 years of operation, Austal has built over 350 vessels for 122 commercial and defense operators in 59 countries.

Market Cap $909.3m AUD or roughly $611m USD

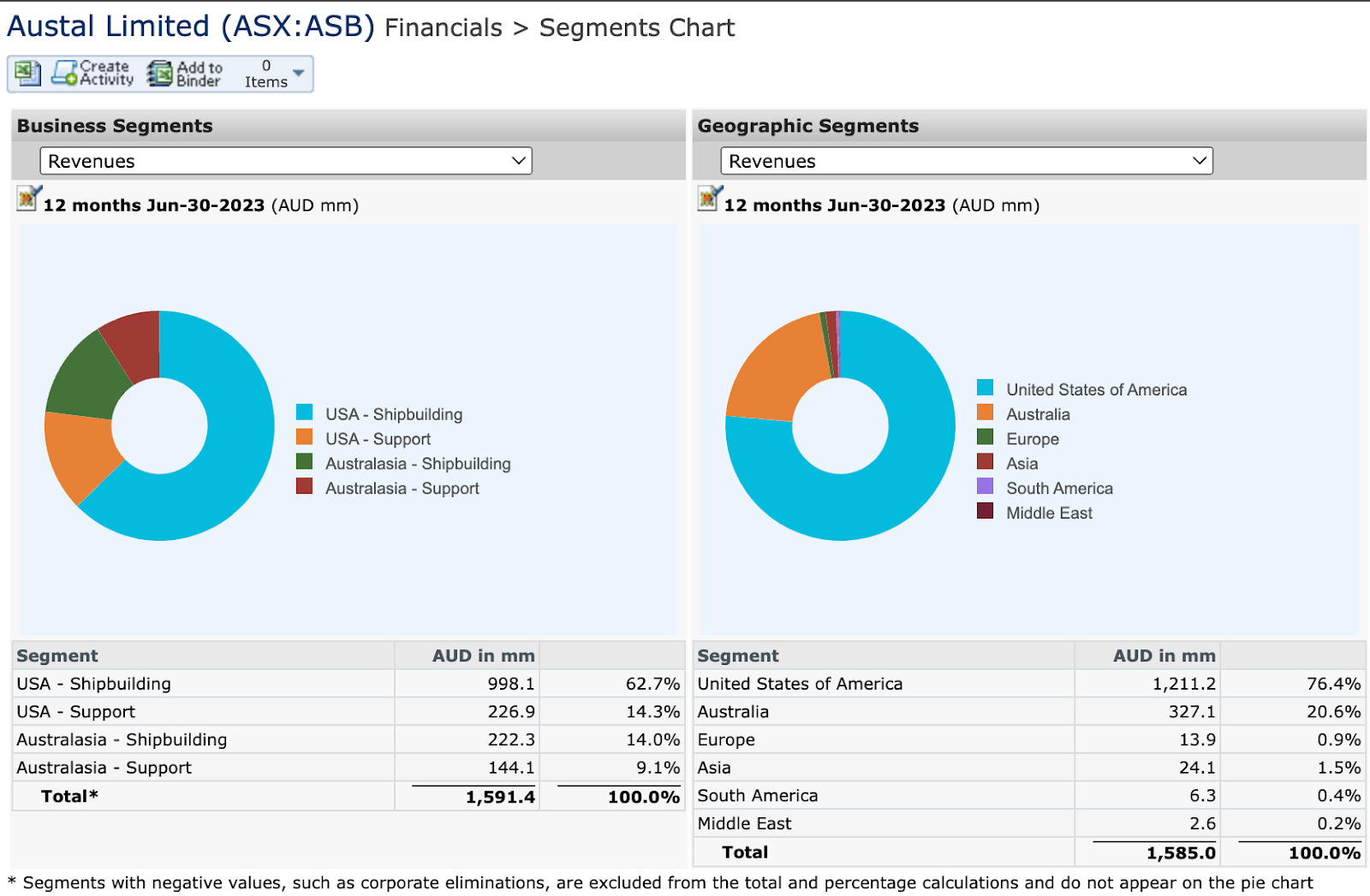

Primary Segments:

Fundamental Financial Data

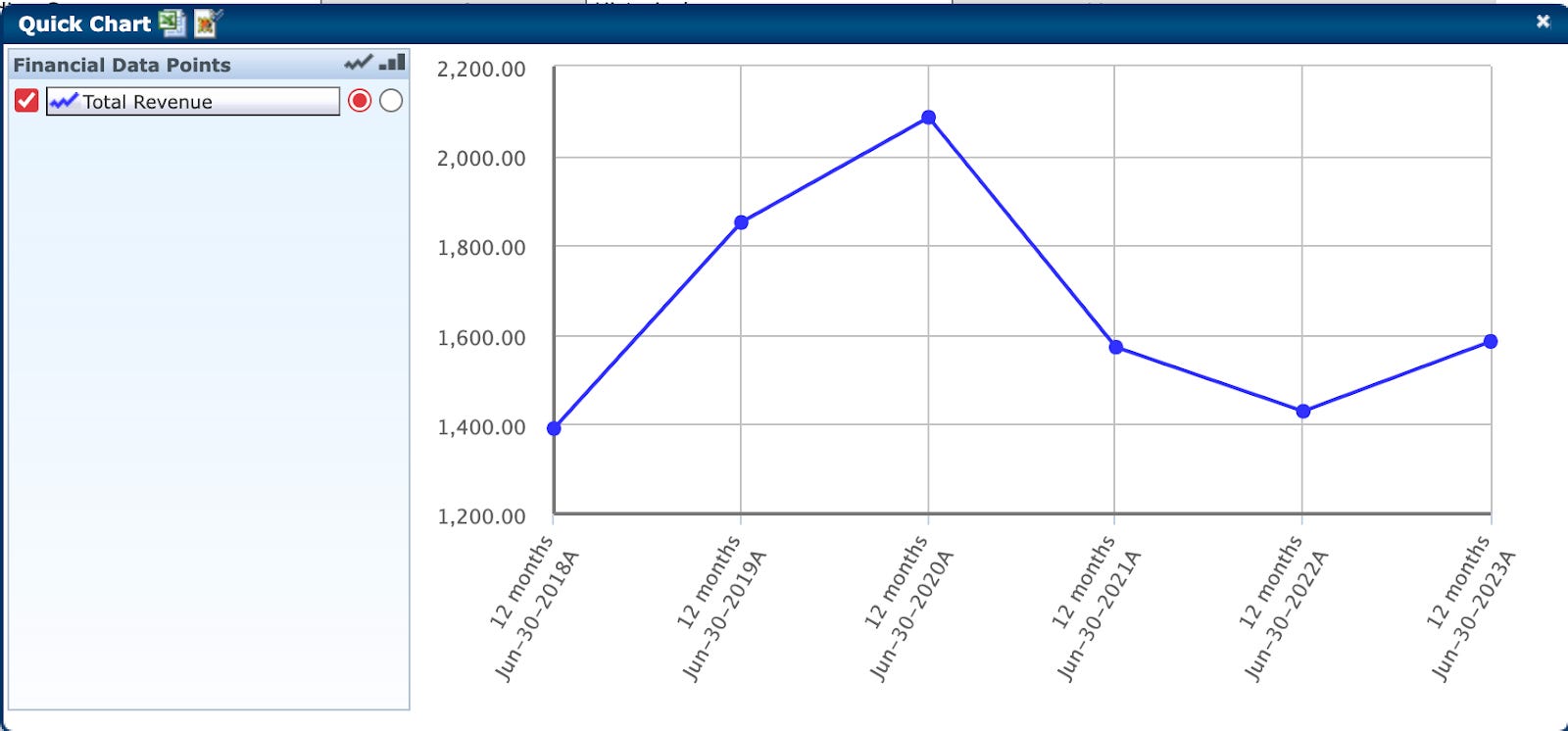

Revenue has only increased 14% since FY2018 – has been highly variable from year to year, but they are projected for strong growth in 2024 and 2025 of 7.98% and 18.80% respectively.

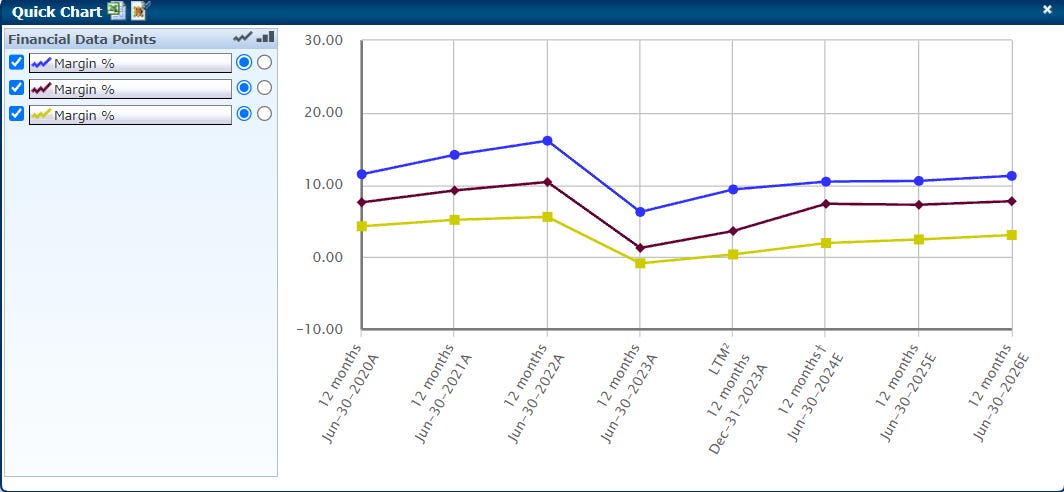

Margins - Margins across the board have historically been much higher than in 2023, but that is seen as an outlier by management due to the specific circumstances regarding the T-ATS contract complications. Given that the T-ATS was their first venture into steel shipbuilding as opposed to aluminum shipbuilding, it may be overly positive to assume that margins significantly improve in future years. The new steel shipbuilding facilities did not meet expected efficiency levels, which led to increased labor hours and higher costs, which the company claims to have made adjustments for.

Debt – Net Debt of $61.3m compared to 2023 EBITDA of $20m results in a relatively high 3.065x leverage ratio, but within EGA’s goal of less than 3.5x

Total debt is trending up; this is the first time since 2018 that Austal has had more debt than cash and short term investments indicating a potentially worsening financial position.

Investment Thesis

The fundamental opportunity/storyline here is the expected race to grow United States and Australian naval capacities and that Austal is positioned to benefit from increased spending in that sector. The belief is that this spending will grow in response to China’s navy becoming the largest in the world. Not only is China’s navy more developed on an absolute basis, they also boast the more technologically advanced navy with most of their ships being launched from 2015-2019, where most of the US Navy’s ships were launched in the 90s and 2000s. For these reasons, it seems like the US will invest heavily in their Navy in years to come.

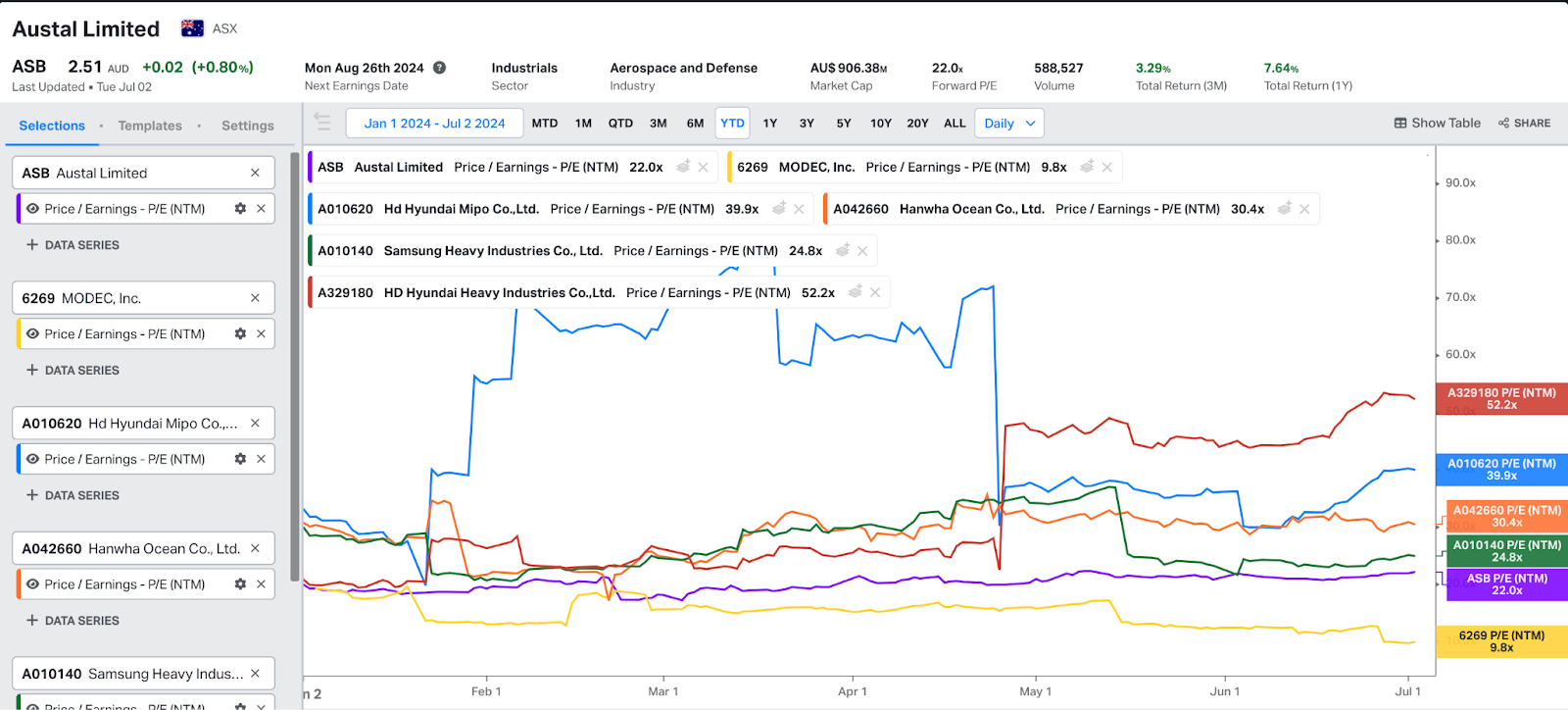

The valuation/investment opportunity seems like an aggressive bet on company specific execution improving along with the rising tide of increased defense spending being a key driver of future growth. The price to earnings ratio of 22x NTM is more than two standard deviations from the company’s historical mean PE ratio. If I had to categorize this company under Buffet’s analogy, right now you are paying a high price for a decent company that is propelled by industry wide growth more than company specific factors. Their ROE (3.4%) is much lower than the peer average of 6.4%, and their margins (2% N/I) are among the lowest of the peer group.

Catalysts / Re-rating potential

Announcements concerning the US Navy’s FY2024 and 2025 budget requests passing Congress

Earnings results (Aug 20) – improved profitability in the steel shipbuilding segment, indicating that management has taken steps to regulate costs and forecast efficiency in this newer business segment – stock could rerate much higher or much lower based on this segment as many of their 2023 contract wins were for steel ships

Main Drivers / Sensitivities

Australia’s overhaul of their naval force is a key driver of the company’s projected growth as $11b AUD is projected to be invested in acquiring/developing new ships and capacities within their navy and growing the overall count of their vessels from 11 to 26 over the next decade

“The U.S. Navy will postpone most of its planned development and purchases of large unmanned systems and next-generation ships and planes in fiscal 2025, citing spending caps”

The Department of the Navy is seeking $257.6 billion for FY25 for the Navy and Marine Corps, up 0.7% from the FY24 request Congress has not passed more than five months into the fiscal year.”

Despite projected spending increases slowing down, the existing budget is already large. Additionally, the company has experienced strong growth in their order book and agreed to multiple US shipbuilding contracts in 2023 (T-AGOS $3.19b, OPC up to $3.3b)

Completed renovations of the company’s San Diego waterfront ship repair center makes 3 in the US Support segment. With new ships being delivered, it is fair to expect continued revenue growth within this segment in 2024 and beyond. (Segment grew from $175.8m in FY2022 to $226.9m in FY2023 or 29% YoY)

Valuation

Currently trades more than 2 standard deviations from NTM P/E mean of 12.4x (Koyfin) indicating that the market is pricing in significant earnings growth

The positive re-rating they’ve experienced is likely due to the projected industry tailwinds and Australia’s announced overhaul of their fleet, but this doesn’t price in risks of lower profitability given one of their latest projects, the T-ATS resulted in a net loss due to poor project forecasting

Peer Group is valued higher on average than Austal (31.42x vs. 22.0x) potentially indicating some company specific risks with Austal

If the risks concerning US budgetary tightening materialize, it is likely that Austal re-rates much closer to their historical average of 12.4x or even lower

Costs

Major reason net income was negative in 2023 was primarily due to a significant loss provision related to the Towing, Salvage, and Rescue (T-ATS) ships program. The factors contributing to this loss included changes in specification, cost inflation pressures, and incorrect efficiency assumptions.

To minimize this risk in the future, Austal has attempted to isolate this issue to the T-ATS project, requested equitable adjustments for recovering additional costs, and released remaining contingencies associated with other mature programs to better manage risks and ensure more accurate financial forecasting in future projects.

ESG

Goal of 50% reduction in Scope 1,2, and 3 emissions by 2030, and Net Zero commitment by 2050.

Launched high speed electric ferry in 2021 for commercial use and that will contribute to their net zero goals in future years

Positives

Largest order book in company history – $11.6 billion (USD)

Highlight of last year was getting the Offshore Patrol Cutter (OPC) program with the US Coastguard for 11 ships at a total value of $3.3billion. Project is still in design phase with cut metal expected before end of FY2024

Complete overhaul of Australian Navy announced in February of 2024, with $11b AUD to be invested in their fleet over the next decade – increasing surface fleet as well as integrating large uncrewed capabilities into their fleet

New Chairman of the Board appointed in June of 2024 is the former US Secretary of Navy Richard Spencer – familiarity and connections to US military is an advantage

The US fleet is older than others, and this may result in more frequent servicing being required which Austal is positioned to benefit from, with 3 service centers in the US

Negatives

Company didn’t manage costs effectively in FY2023 resulting in a net loss of AUD $13.77m primarily due to a significant loss provision of $171.2m related to the Towing, Salvage, and Rescue (T-ATS) ships program. The factors contributing to this loss included changes in design specifications, cost inflation pressures, and incorrect efficiency assumptions.

Australian political dissent within the defense sector could slow progress and become a headwind for the company’s 3rd largest segment – feels as though market is not pricing that in at a 22x PE ratio

Australia’s plan to increase their fleet of ships and subs is longer term – the last of the planned ships is to be delivered by 2043. It could take longer than expected for these planned investments in defense to materialize into cash flows to the firm

Upside Risks

Positioned to benefit from rising global tensions which will increase spending on the defense sector

Increased pressure from China’s investment in naval resources is a tailwind for Australian and US spending on shipbuilding (China’s navy is currently the largest in the world per International Institute for Strategic Studies)

Downside Risks

Tensions between defense minister Richard Marles and defense establishment could lead to impacted completion of agreed upon projects and affect defense spending budgets (Australia’s Shadow Defence Minister called the overhaul plan “superficial” and claimed there was no “larger strategy”)

Execution risk within the Australian defense sector: an audit office review of major defense projects found there was a “cumulative blowout of over 37 years in completion dates of major projects”

A pivot in military tech towards nonconventional types of warfare (drones, cyberattacks, etc.) could be a headwind for the company. Ukraine has had success using unmanned maritime drones packed with explosives against the Russian fleet and other countries could utilize these strategies instead of spending on the larger ships that Austal specializes in.

Sources (Turn into PDFs)

https://www.rferl.org/a/ukraine-navy-black-sea-russia/32826343.html

https://investor.austal.com/static-files/80bbc558-4bd5-4fad-b3b1-79eee9141880

https://www.csis.org/analysis/unpacking-chinas-naval-buildup

Images