Stock Research #2: Qinetiq

Date of Research: 6/28/24

6/28/24 Close: $22.53

9/26/25 Close: $28.50

Total Return: 26.51%

CAGR: 20.6%

Qinetiq Research Sheet

Company Description

Qinetic is a science and engineering company operating in the security and defense industry. The company offers advisory, consulting, cybersecurity, mission data, robotics, etc. The company’s primary segments include EMEA Services and Global Solutions.

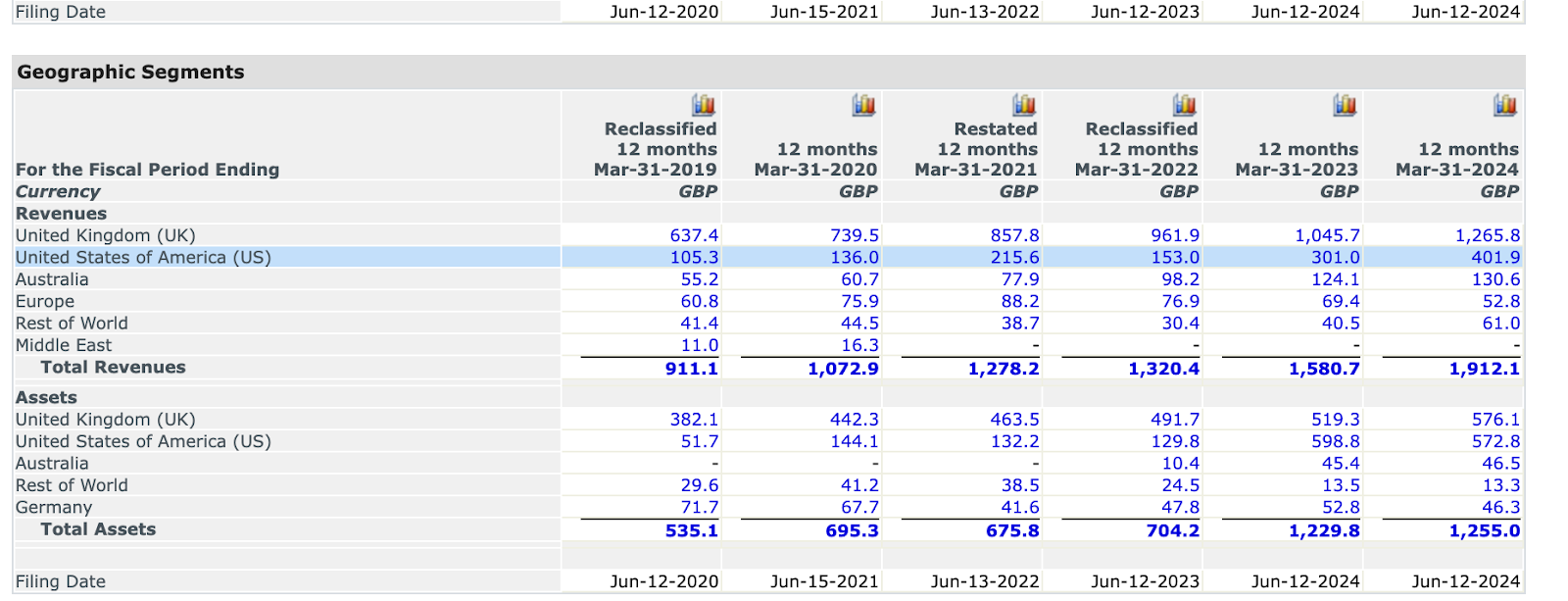

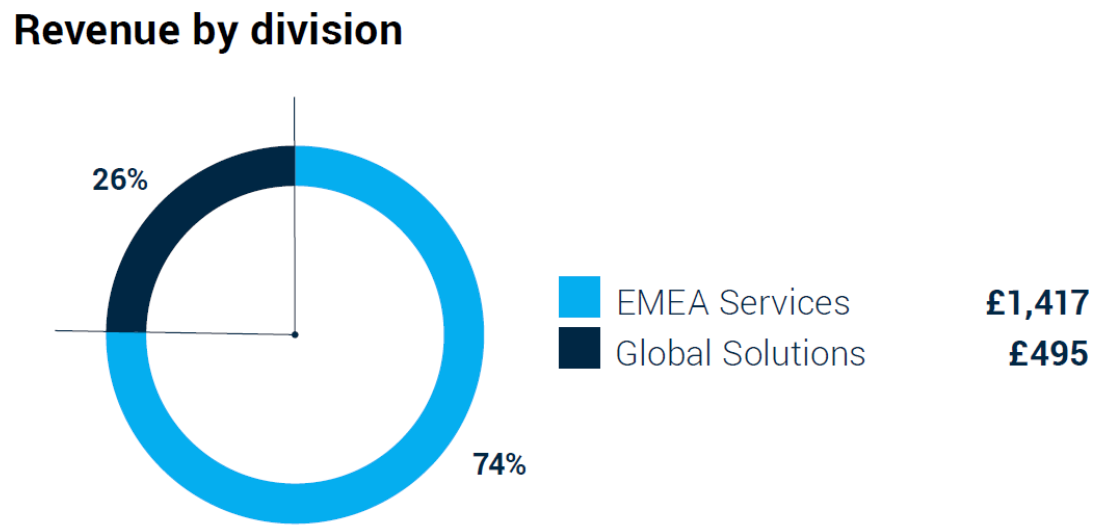

Revenue Breakdown:

Investment Thesis

Qinetic is well-positioned given a recent rise in geopolitical tensions, namely conflict in Eastern Europe and the Middle East. Qinetic has long-term contracts with multiple countries involving existing and new product lines.

Qinetic’s core business generates stable cash flows with high single digit profitability. They have a reliable long-term contract base and favorable R&D subsidies provided by the governments they work with. Qinetic’s ROE is strong, driven by an asset turnover ratio (0.92) that is more favorable than its peers (average 0.6)

Catalysts / Re-Rating Potential

Delivering on the guided high single digit organic revenue growth promised in annual meeting, as well as increasing net income to 5-year historical average of 8.66% (compared to FY24 mark of 7.3%, which would have resulted in an almost £26m difference in net income in FY24 – roughly £470m of value at 18x earnings)

Recently named as prime supplier of 2/6 lots in £1.2b Digital and IT Professional Services framework by the UK’s Ministry of Defence, as well as a subcontractor of a separate 2/6 lots

Began £100m in share repurchases in January 2024, £16m of which was already bought back by the end of March

Recently increased dividend growth rate from 5% to 7% reflecting their confidence in future earnings growth

Main Drivers/Sensitivities

20% organic growth in EMEA services segment of the business driven by delivering on the two major agreements with the UK’s Ministry of Defence (MOD)

The Engineering Delivery Partner Agreement (EDP)

Has resulted in over £1.5b of orders since agreement inception in Dec. 2018

The Long Term Partnering Agreement (LTPA)

Extended through 2033

Positioned to benefit from the UK’s investment in the dragonfire laser technology used to shoot down drones at a lower cost than conventional missiles at a lower cost. (£10 per shot vs. current missile cost of $2000-$4000) Dragonfire will be installed on all of the Royal Navy’s ships by 2027. This system helps minimize space requirements for missiles.

Currently capable of targeting a coin sized object at 1km range

Main Driver of US Growth in the past two fiscal years has been through the Avantus acquisition finalized in 2023, where 75% of their new US contracts have been from this acquisition

Further investments in monitoring the US-Mexico border could be an area for growth as Qinetiq already has contracts with the US government for this service of employing tethered aerostats to monitor the border in real time ($170m TARS contract awarded in Nov. 2023)

Valuation

Trades at 18x TTM EPS – in line with peer group

9.1x EV/EBITDA is cheap compared to the peer group (13.0 average, 12.4 median)

With the higher DuPont ROE that Qinetiq has (17.8%) compared to its peer group average of 12.1% and median 12.9%, could say it deserves to trade at a premium to its peers

Costs

Increased net interest expenses in past two fiscal years due to acquisition of Avantus (£6.5m FY23, £15.3m FY24)

Only £12.8m of the total £328.2m (~4%) of R&D expenditure was internally funded, with the rest funded via their customers, (UK MoD and other governments) so they have a really advantageous cost structure through collaboration with governments to deliver products and services.

ESG

“We saw a decrease in our Scope 1 and Scope 2 emissions in FY24 compared with FY23, equating to a 33% reduction against our re-baselined FY20 base year.”

“Our Net-Zero plan includes a near-term target of 50% reduction in Scope 1 and 2 emissions by FY30 from a base year of FY20.”

Promise of Net Zero by 2050 or sooner

Positives

In November of 2023, Qinetiq was awarded US government contract worth $170m (£133m) with the goal of increasing border security and the fight against drug trafficking into the US (TARS)

£1.74b order intake 2024, 21% rev. growth, and 20% operating profit growth, $1.3b of total contract awards in the US

Steady cash flows from government contracts allow for a £100m share buyback program, 7% YoY dividend growth (1.84% yield)

66% of their EMEA revenue is comprised of single-source contracts which are seen as more steady and recurring as there is no competitive bidding process

Agreements with UK government through 2033

Low risk profile (0.56 Leverage Ratio < EGA’s Target 3.5x or less)

Negatives

$977m of the $1.3b (75%) in grants awarded within the US were from the Avantus acquisition – unsustainable growth

Revenue ex-Avantus acquisition in the global segment was flat YoY

Upside Risks

Potential escalation in global conflicts could prompt increased government spending on defense (In the US, the Research, Development, Test and Evaluation (RDT&E) budget is the largest ever at $145bn)

Potential for anticipatory spending on defense given heightened geopolitical tensions

Downside Risks

Global debt burden may prompt governments to tighten fiscal policy in favor of reduced spending, which could negatively impact defense budgets

While increased global spending on defense is a tailwind for Qinetiq, if they aren’t making advancements constantly, their market share could erode due to other well positioned firms within the sector with more advanced technology

Misc Sources

https://www.qinetiq.com/en/news/us-customs-and-border-protection-has-awarded-tars-to-qinetiq-us

https://www.usaspending.gov/recipient/39259f00-4e82-79ef-4e26-bdb23d6bfb10-C/latest

https://www.qinetiq.com/en/investors/investor-overview

https://www.qinetiq.com/en/news/qinetiq-group-plc-fy24-third-quarter-trading-update

https://www.qinetiq.com/en-us/news/qinetiq-us-to-acquire-avantus-federal

https://www.csis.org/analysis/cost-and-value-air-and-missile-defense-intercepts

https://www.qinetiq.com/en/news/dragonfire-laser-achieves-another-uk-first

Images