SpaceX IPO: Retails Role as Exit Liquidity

6/11/2026

The Biggest IPO in History Lists Tomorrow. I’m Passing.

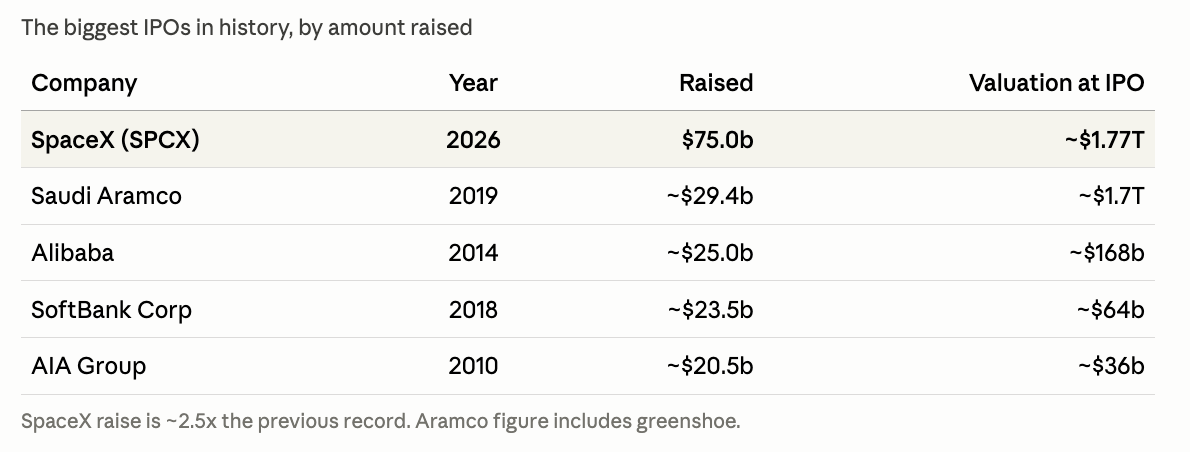

SpaceX is set to IPO tomorrow in what will be the biggest IPO in history, at least for now. Anthropic and OpenAI appear to be close behind.

The numbers: $135 per share, 556.6 million shares offered, a $75 billion raise at a $1.77 trillion valuation. Only about 4% of the company will actually trade.

With a float that small, and retail interest of around $70b before the open, I expect a lot of volatility. Reported total demand sits somewhere between $150b and $250b, depending on who you ask. My guess is it trades well above the $135 listing price.

For scale: the previous record holder was Saudi Aramco, which raised about $29b in 2019. SpaceX is raising roughly 2.5x that in one shot.

The Numbers

In 2025, SpaceX did $18.7b of revenue and lost $4.9b. So the company is coming public at nearly 100x trailing sales while losing money. There is no P/E multiple because there is no E. If you want to be generous and use 2025 adjusted EBITDA of $6.6b instead, you’re still paying about 265x. Back of the envelope: if SpaceX handed shareholders every dollar of that EBITDA forever, it would take more than two and a half centuries to earn back the purchase price.

Of course, the market is forward looking. So we should be too.

Where the Revenue Comes From

Two things matter here: Starlink and, as of about three weeks ago, datacenters.

Starlink is the real business. The connectivity segment did $11.4b of revenue in 2025, up roughly 50% year over year, with $4.4b of operating profit. Profitable, recurring, growing. If this IPO were just Starlink at a reasonable price, I’d be interested.

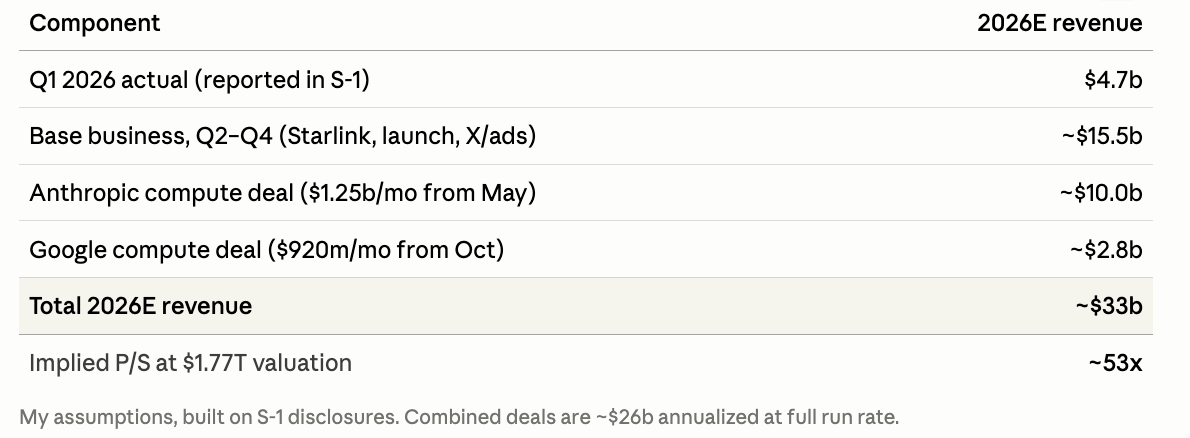

The datacenter side is what’s carrying the valuation. The S-1 disclosed that Anthropic agreed to pay $1.25b per month through May 2029 to rent the entire output of the Colossus datacenters. Then last week, days before the IPO, Google signed on at $920m per month through June 2029 for roughly 110,000 NVIDIA GPUs. That is about $26b of annualized compute revenue from two customers, signed within weeks of the listing.

SpaceX announced Q1 2026 revenue of $4.7b. Add the Anthropic and Google deals, which would bring in roughly $13b over the rest of the year, then layer in the base business. You get to roughly $33b of 2026 revenue.

With those assumptions, the IPO is priced at about 53x current year sales. Again: sales, not earnings.

Paths for Growth (and Why the Growth Is Fragile)

76% year-over-year revenue growth looks great, but most of it comes from the Anthropic and Google deals. The question is whether SpaceX can keep building compute at this pace and rent it out at top-of-market rates while everyone else is also trying to sell GPU capacity.

Based on the S-1, SpaceX could have 300-500MW of compute online and leasable by mid-2027. At current rates, that could bring in $500m to $1b per month. In the rosiest scenario, call it $6b of incremental revenue in 2027. The problem is that NVIDIA will also be shipping GPUs to CoreWeave and the hyperscalers over that same period. Supply goes up.

And then there’s concentration. Two customers account for essentially all of the incremental growth, and the S-1 names both of them as competitors.

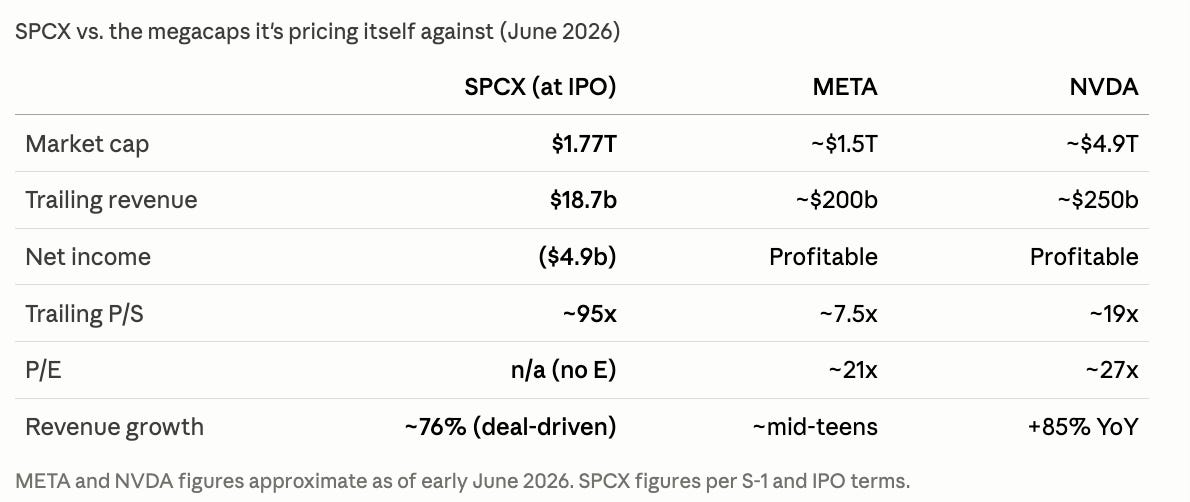

Comparison to the Megacaps, Specifically $META

This is the part that gets lost in the headlines. SpaceX is listing above Meta’s current market cap. Meta does roughly $200b in revenue at around 50% EBITDA margins and trades around 18x forward earnings. SpaceX did $18.7b and lost money.

You’re being asked to pay more than Meta’s price for about a tenth of the revenue and none of the profit. Both companies are spending enormous sums on AI. Only one of them generates the cash flow to pay for it internally.

What You Have to Believe at $135

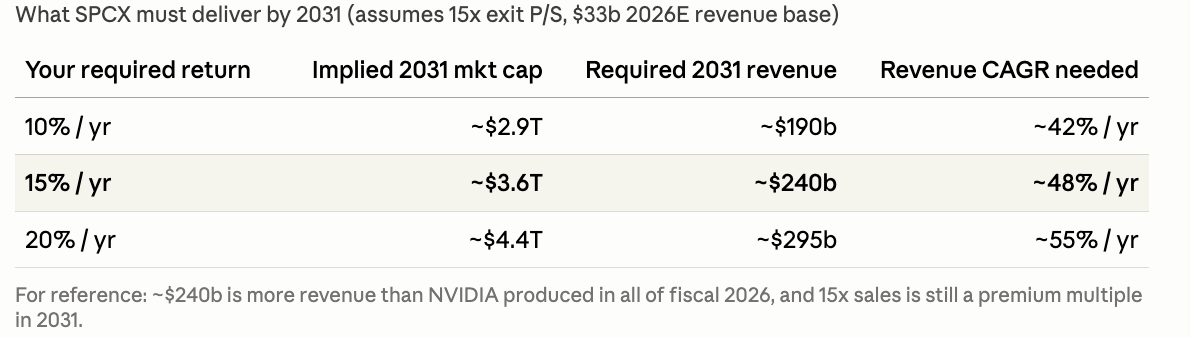

Let’s reverse engineer the price. Say we assume a 2031 P/S multiple of 15x, which would still be a big premium to most companies, and a 15% annual return over the next five years. SpaceX would have to maintain roughly 50% revenue growth every single year, reaching about $240b in revenue in 2031, just to make those assumptions work.

And that is only for a 15% annual return. My guess is plenty of retail buyers tomorrow are mentally underwriting something much higher than that.

The Index Inclusion Game

The float is small on purpose, and the whole structure looks built to get into the indices quickly. Under new Nasdaq rules effective May 1, a company of this size can enter the Nasdaq 100 within about 15 trading days of listing instead of waiting a full quarter. FTSE Russell has cut its window to 5 days. BNP Paribas estimates roughly $8b of forced passive buying in the first month from Nasdaq 100 inclusion alone, and something like $30b of total passive demand across the index families. If you own a Nasdaq 100 fund in your portfolio, you’ll own SpaceX within weeks whether you wanted to or not.

The xAI Escalator

It’s worth being clear on who gets liquidity tomorrow. In 2022, a group of co-investors helped Musk take Twitter private at $44b. By 2024, some of those stakes were marked down roughly 70%.

Then xAI absorbed X in March 2025 at an $80b xAI valuation, converting their underwater social media bet into hot AI startup equity. Then SpaceX bought xAI in February 2026 in an all-stock deal that valued xAI at $250b.

Tomorrow, those SpaceX shares start the clock toward being publicly tradeable.

So the 2022 Twitter co-investors rode an escalator from a deeply impaired social media position to liquid stock in a $1.77 trillion public company. This IPO is the top floor.

Retail FOMO Is the Product

30% of the offering is earmarked for retail, roughly triple the normal allocation for a deal this size, distributed through Fidelity, Robinhood, and the big retail channels. The headlines have done the rest. Demand of $100b against $75b offered.

When a deal is built to maximize retail participation and the float is deliberately thin, you should ask who the structure serves.

Yes, It Can Obviously Pop

To be fair to the bull case: thin float, oversubscription, forced index buying, a retail base that won’t sell on day one, and the Musk premium. This thing can absolutely rip in the short term. I would not be surprised to see it trade well above $135 out of the gate. Some are already betting the day-one close lands above $2 trillion.

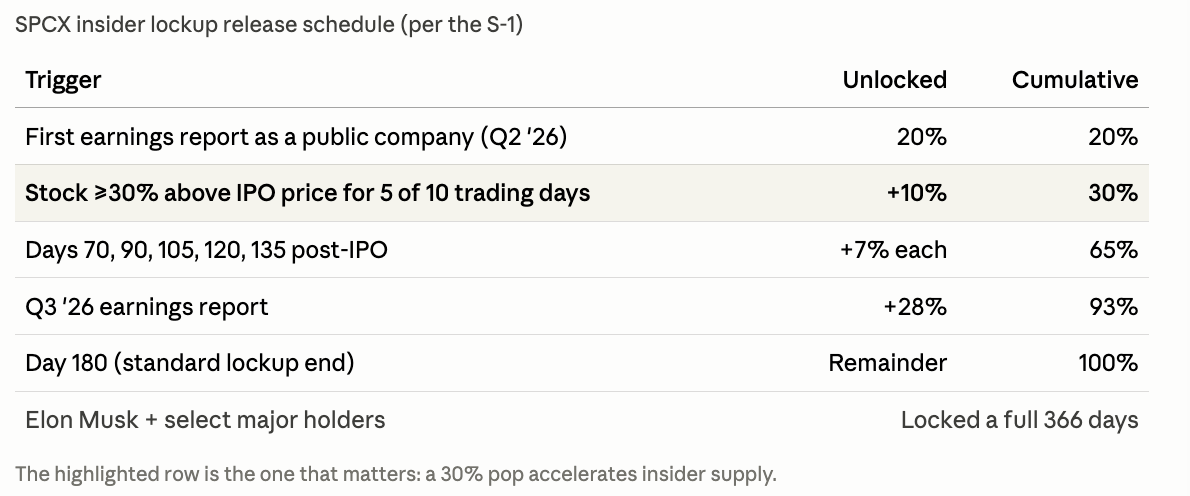

The Near Term Selling Pressure

Additionally, the lockup structure rewards the pop with supply.

After the first earnings report as a public company, insiders can sell 20% of their eligible shares. If the stock is also trading at least 30% above the IPO price for five of ten trading days, they unlock an additional 10% on top. Then 7% tranches release at 70, 90, 105, 120, and 135 days. Another 28% unlocks after Q3 earnings, and the remainder frees up at the standard 180 days. Musk himself is locked for 366 days, which matters. But everyone else gets out early, and faster if the stock goes up.

The Trade

Most of SpaceX’s growth, at least in this version of the story, comes from the compute deals. Compute supply is growing quickly, and that could pressure rates. Maybe demand keeps growing fast enough to absorb it. But if that’s the bet, NVDA looks like a cleaner way to express it than SPCX.