What Happens if Netflix Owns HBO?

$NFLX as an asymmetric opportunity with 25% downside vs 100% upside

Warner Bros. Discovery: Recent Context

Before discussing Netflix as an investment opportunity, it is worth establishing the background of the company it is in the process of acquiring, Warner Bros. Discovery (WBD).

WBD was formed through an April 2022 merger between WarnerMedia (HBO, HBO Max, Warner Bros. Pictures, DC Entertainment, CNN, TBS, TNT, and Cartoon Network) and Discovery (Discovery Channel, HGTV, Food Network, TLC, Animal Planet, and Discovery+).

In June 2025, WBD announced plans to separate into two independent entities: a Streaming & Studios division (Warner Bros., HBO, DC Studios) and a Global Linear Networks division (CNN, Discovery, and related assets).

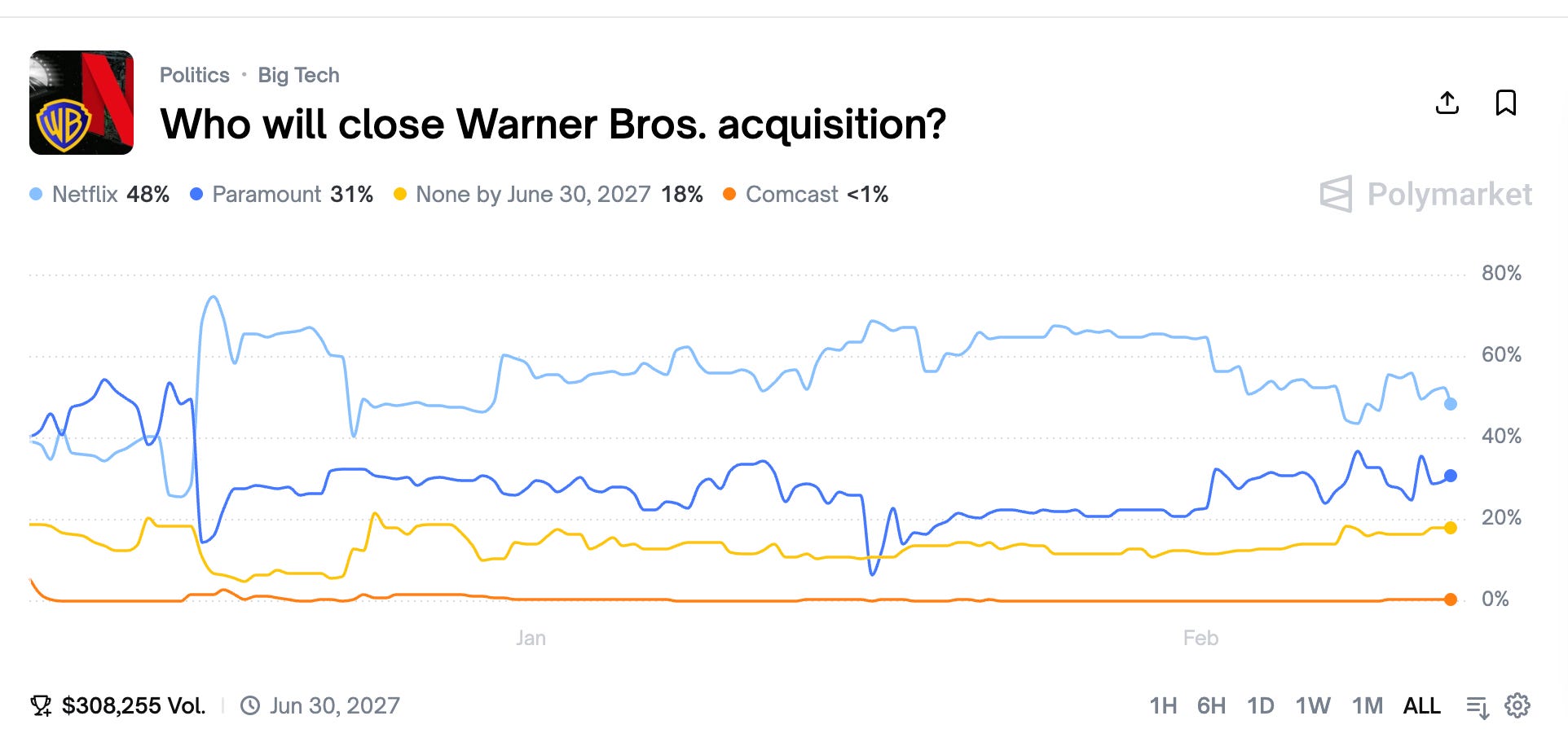

By December 2025, WBD had entered into an agreement to sell its Streaming & Studios division to Netflix for $82 billion. Paramount Skydance made multiple counter-bid attempts(for the entire company), and as of February 11th has raised its tender offer to $108 billion, including a commitment to cover the breakup fee should WBD walk away from the Netflix deal.

The distinction worth highlighting is that Netflix is selectively acquiring the Streaming & Studios division, the higher-value assets, while Paramount’s bid encompasses the entire company, including the Global Linear Networks segment.

In my view, Paramount’s offer appears less strategically motivated and more reflective of a need to maintain competitive relevance in the streaming landscape. Paramount has also attempted to frame the Netflix acquisition as an antitrust concern, positioning its own bid as a more regulator-friendly alternative by pledging to keep WBD’s entities operationally separate.

From Netflix’s perspective, the real value lies in the intellectual property housed within the Streaming & Studios division — franchises like DC Comics, Game of Thrones, and Dune. Netflix appears to have a clearer strategic rationale for how these assets integrate into its business, and that clarity of vision is a meaningful part of why I find the company compelling as an investment, particularly following a significant downward re-rating.

Investment Thesis: Growing their Audience & Increasing Customer Retention

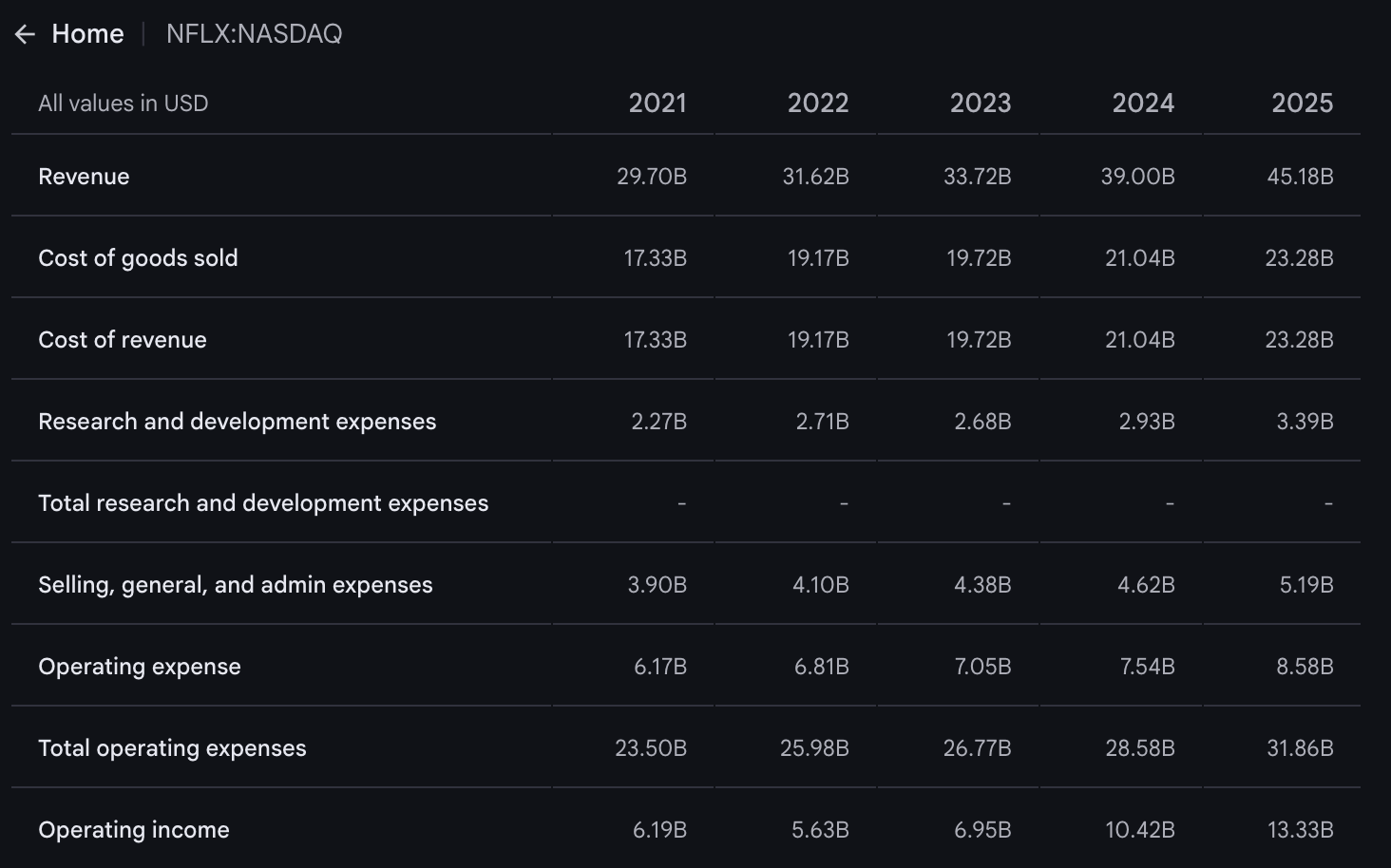

Netflix’s core business has been steadily growing over the years. Their revenue in the fiscal year ending December 31, 2021 was $29.7 billion, and over the past four years it has grown to over $45 billion, at a CAGR of 11%.

Looking to the future, Netflix has decided to invest in acquiring intellectual property via the WBD acquisition that they really haven’t had in the past outside of the hit show, Stranger Things. I think this makes sense, as the problem with subscription based companies like Netflix, is that they will lose a lot of users to churn when shows like Stranger Things stop airing.

By acquiring WBD and its intellectual property, which includes hit shows like Game of Thrones, Netflix protects itself from churn while growing the audience of people who would want a subscription to their favorite shows and movies.

They protect the user base that they already have, while growing it substantially, and they also gain the ability to package HBO Max and Netflix at a cheaper price to consumers, similar to the Disney+/Hulu business model.

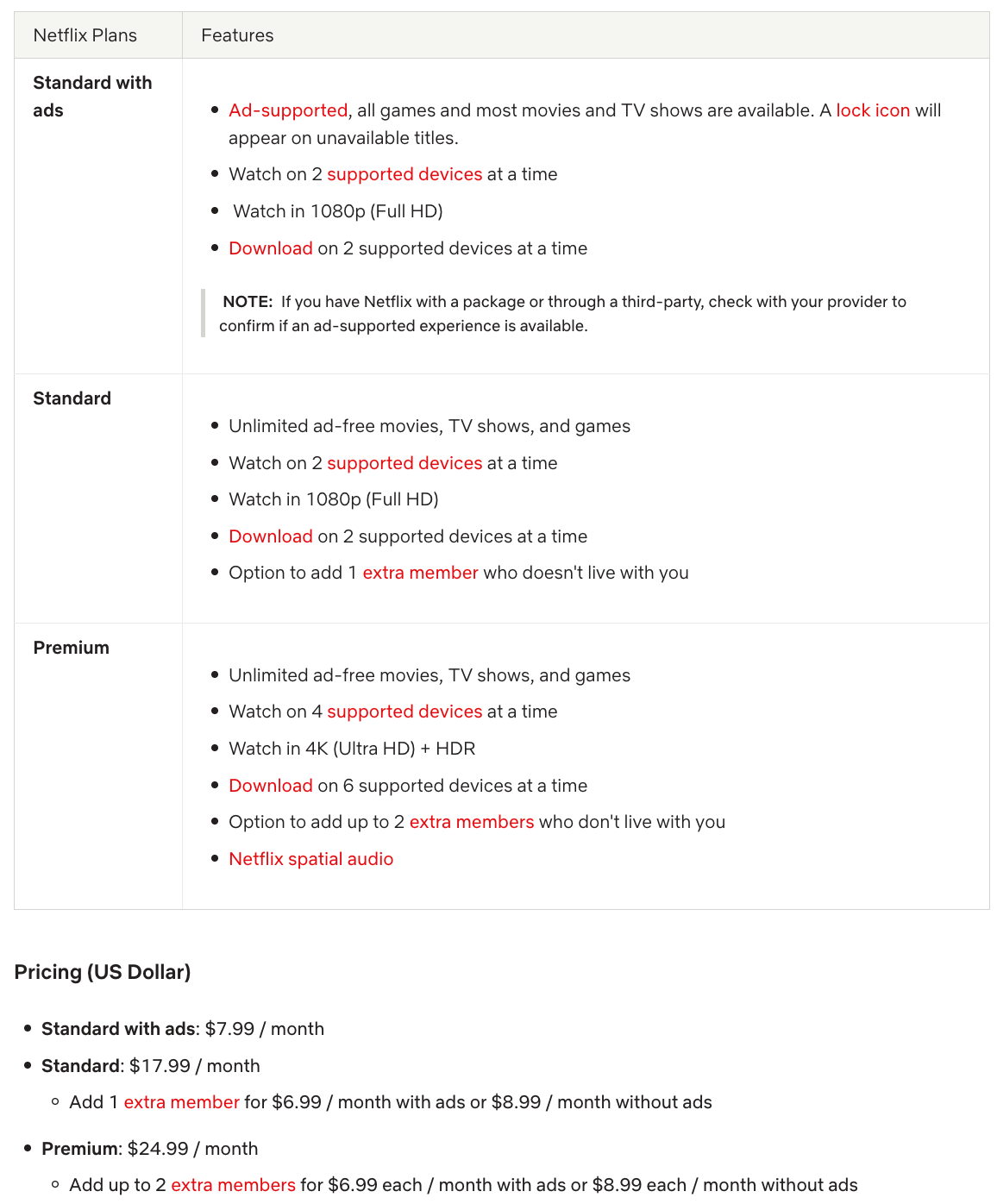

I believe that Netflix truly knows how to monetize streaming, as they have multiple tiers of subscriptions with and without ads, and have largely been able to crack down on password-sharing. If they can continue to dominate popular culture and acquire fan favorite shows and movies, they can increase their pricing power as well as the stickiness of each subscriber.

In addition to this, I believe there is a tail outcome in which movies quickly go from theaters to in-home streaming, and that Netflix is going to be a major driver of this. The CEO has already said that he wants movies to go from theaters to streaming quicker, claiming that it’s not ‘consumer-friendly’ to have long exclusive windows.

If Netflix can actually make this happen, especially with DC Studios as part of their library, I think this would drive a lot more revenue to them. From a unit economics perspective, the movie theater experience (~$20/ticket, family of four so ~$80 in tickets + $15-25 in terms of snacks/candy) is much more expensive than the $20-25/month streaming costs. If movies hit streaming within a few weeks of being released I think Netflix could really take market share from in-person moviegoers.

DC Studios could also be a major driver of revenue for Netflix, as we saw the MCU was a major financial boon for Disney in the late 2010s, and the DC’s version of that is just ramping up since the initial Superman movie released in mid-2025. I think that DC Studios is being run very well by James Gunn, and it's a major positive for the future of DC Studios that he was such a large part behind the success of Marvel’s Cinematic Universe in the late 2010s.

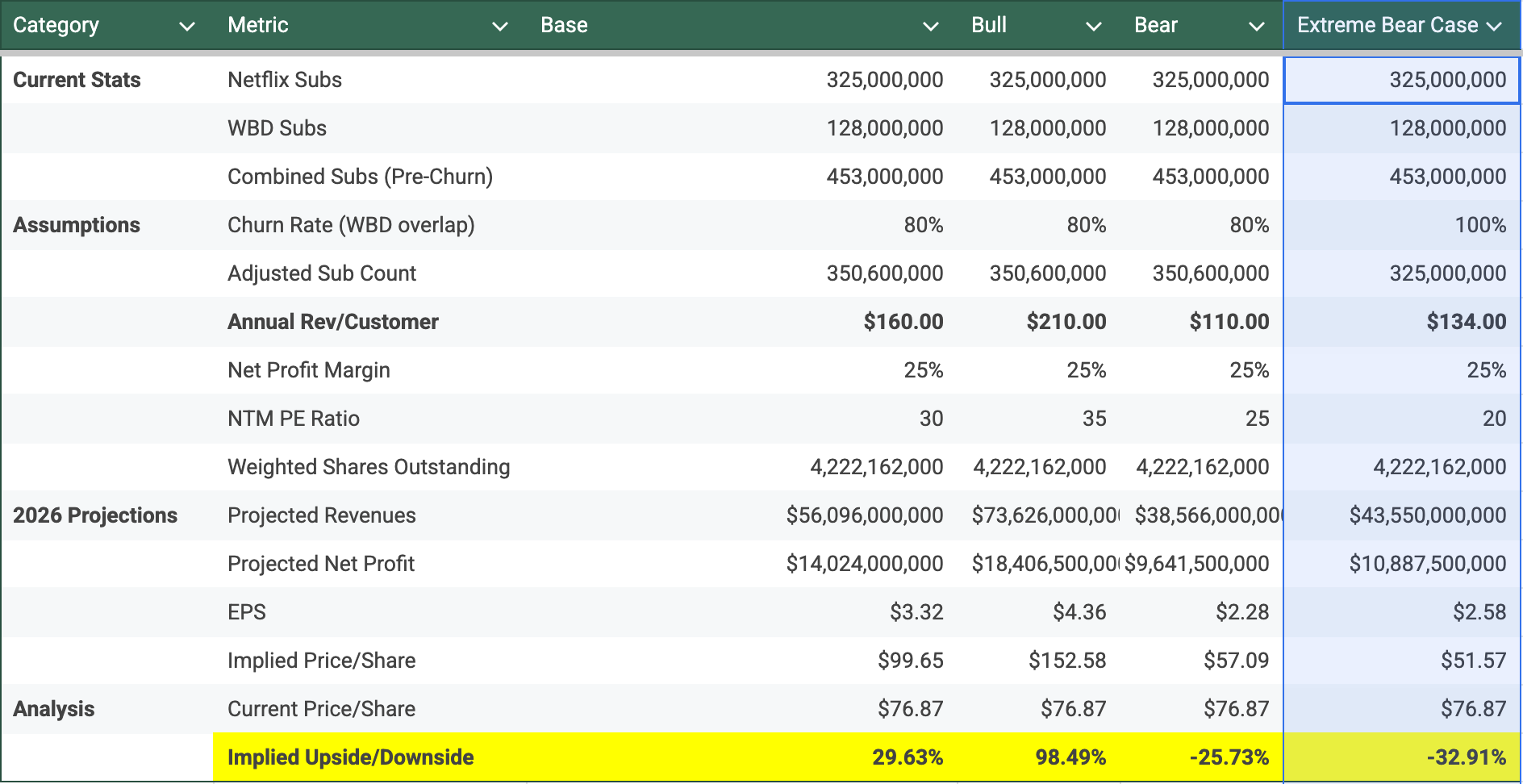

Back of the Envelope Math: What’s the Upside?

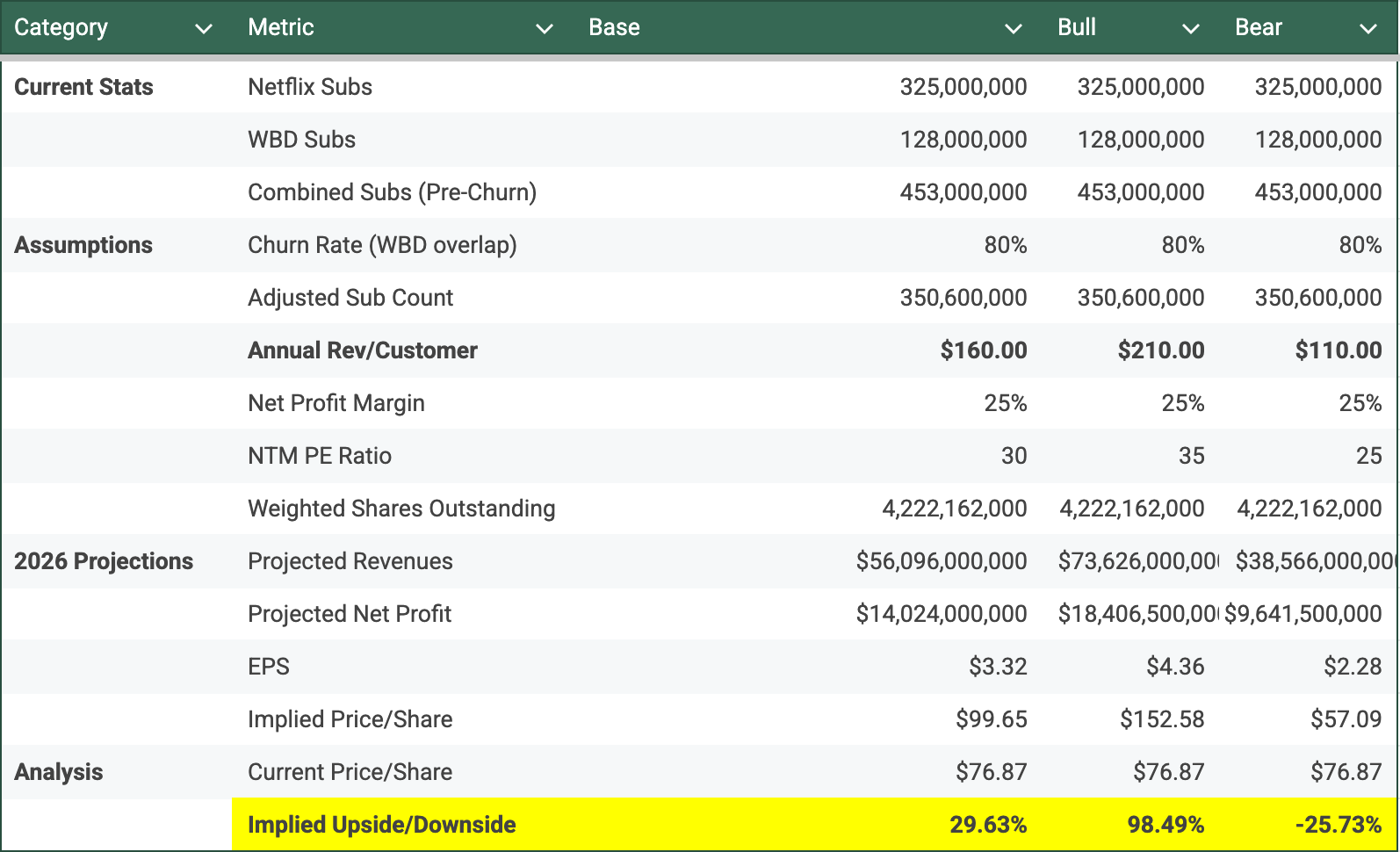

Just for fun, I thought I’d do some back of the envelope math to see what Netflix’s earnings/valuation could look like in certain scenarios.

In terms of my assumptions, I believe they are defensible and I will try to explain each one in detail here.

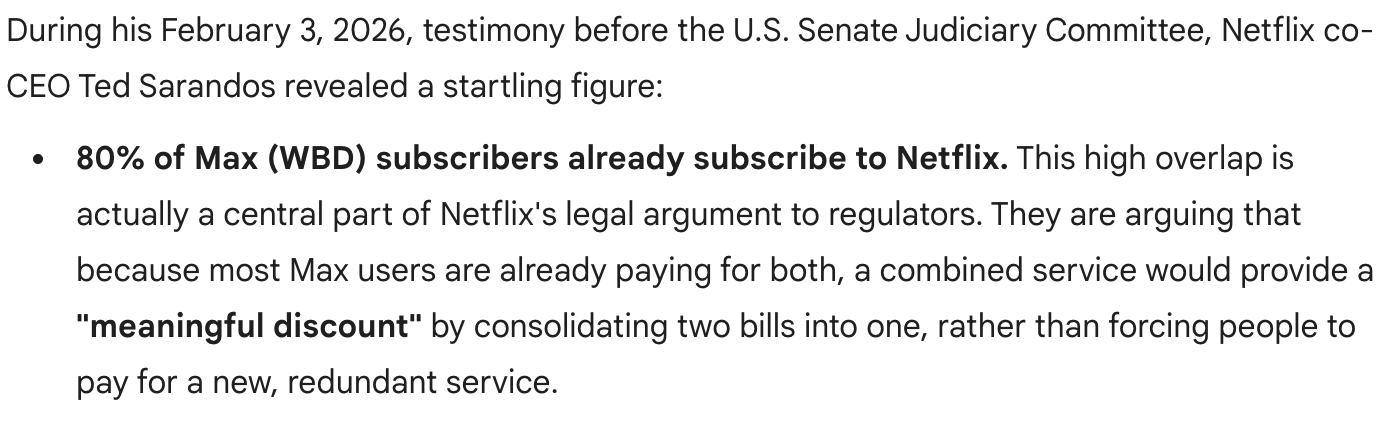

Churn Rate (WBD Overlap) refers to the amount of WBD users who already have a Netflix sub. This figure is from Netflix themselves, and is part of their legal argument to regulators. More below:

Adjusted Sub Count is taken by adding Netflix subs (325m) with WBD subs (128m) and subtracting the amount of WBD subs who would remove a sub because they already pay for Netflix. This is done to avoid double-counting.

Annual Rev/Customer is where I think this trade comes to life. If you average out the annual rev/customer from Netflix ($134) and WBD ($85) you get ~$110. I put this as the bear case to be conservative, but I think it’s highly unlikely that Netflix doesn’t raise prices if this deal goes through.

I think an average revenue per user of $160/year or $13.33/month is entirely reasonable, especially considering the increase in content provided with that subscription. This would be a 19% increase from Netflix’s current annual revenue per user.

In the bull case, I put $210 as the ARPU, as this would be a massive increase in subscription cost, but Netflix may have the pricing power to pull this off.

Considering that 80% of WBD subscribers feel that they can afford both the $134/yr for Netflix and the $85/yr for WBD, totaling $219/yr, maybe paying $210 isn’t that crazy?

Net Profit Margin I assumed to be stable because Netflix has operated in the streaming business for years and I don’t expect that this acquisition will materially affect costs.

NTM PE Ratio I believe will increase from 25 to 30 in the case that this acquisition goes through, and if Netflix can successfully monetize their combined product of Netflix and WBD, I think it could even re-rate to 35+.

I think based on these assumptions, Netflix provides an asymmetric opportunity — -25% downside with upside to ~100% in returns over the next few years.

It’s important to note that these scenarios all assume the acquisition goes through successfully which is not a given. They also do not take into account the benefit of natural subscriber growth that is expected of these companies.

Near Term Catalysts

While I don’t necessarily disagree with the antitrust concerns, if this deal does pass, I think Netflix will definitely have an even more dominant position within the streaming space. With IP like Dune, Harry Potter, Game of Thrones, and DC Studios, and Netflix’s belief that the gap between a movie releasing in theaters and going to streaming will close, I think that we’re going to see even more people just skip the theater and decide to wait till the movie hits streaming. See co-CEO Ted Sarandos’ comments below.

It is important to note that while I believe the acquisition will go through, traders on Polymarket have the odds at only ~50% that Netflix will be the company to acquire Warner Bros by mid-2027.

This acquisition and any legal developments on it are definitely going to be catalysts for Netflix as a company. While I like this acquisition a large part of my investment thesis, I do not believe there is significant downside if it falls through given Netflix’s large pre-existing business, especially from this slightly depressed valuation.

The shareholder vote on the Netflix/Paramount acquisition debacle is likely going to be in mid-late March, so I would expect clarity on the situation by at least April, but the legal process could take much longer. Especially considering David Ellison (CEO, Paramount), the son of Larry Ellison (CTO, Oracle), are lobbying to Trump that the acquisition by Netflix should be blocked, citing the aforementioned antitrust concerns.

Costs

From 2021 to 2025, operating margins have gone from 20.8% to 29.5% respectively, signifying that NFLX 0.00%↑ has been able to keep costs under control while ramping up revenues. Given that their levers to pull in terms of revenue drivers are increasing subscription costs + event-style content, this makes sense intuitively.

I think in terms of costs you should be watching, it’s really just cost of acquiring new content. While Disney/Hulu+ is a competitor to Netflix, I think their main competitor is YouTube.

The reason YouTube stands out to me is that YouTube’s content is primarily user-generated, meaning that they are not undertaking any costs besides the service of hosting all of this content. This means that their job is just serving the right content to the right consumer, and keeping that consumer on platform for as long as possible.

So, in that same vein, as investors in Netflix, the cost you really want to watch are the costs of acquiring new content, which this acquisition is doing. Does acquiring WBD 0.00%↑ and getting content like Game of Thrones, DC Studios, Harry Potter, etc. drive new users, and maintain them over time? My answer to that question is yes.

With the release of HBO’s newest Game of Thrones spinoff, A Knight of The Seven Kingdoms, my Twitter, YouTube shorts, Instagram Reels, etc. timelines have been full of content about the show, with millions of impressions on each post. Game of Thrones’ other spinoff, House of the Dragon also is expected to release mid-2026.

Additionally, DC Studios has Lanterns coming out in the summer of 2026, and HBO Max also has a Harry Potter show coming out in early 2027.

With all of these different IPs releasing year round, you have to think subscribers will opt to pay for the annual subscription, saving slightly on subscription fees, but reducing the churn that naturally comes with streaming services.

The acquisition of WBD and these assets makes sense because it truly offers Netflix to have a full calendar of content releasing, which would materially reduce both churn and the seasonality of revenues around shows like Stranger Things.

Costs and Debt of Acquiring Warner Bros. Discovery Streaming Division

A key concern is the debt load Netflix is taking on with this acquisition. Netflix is taking on $42b bridge financing for this deal, and has paused share repurchases.

This is likely a large part of their re-rating downwards, but I think investors are missing the forest for the trees here. Companies make investments in the expectation that future revenues will pay for them multiple times over. I believe that Netflix’s investments into this differentiated IP and content library is worthwhile and I do think it’ll pay off in the years to come.

Valuation

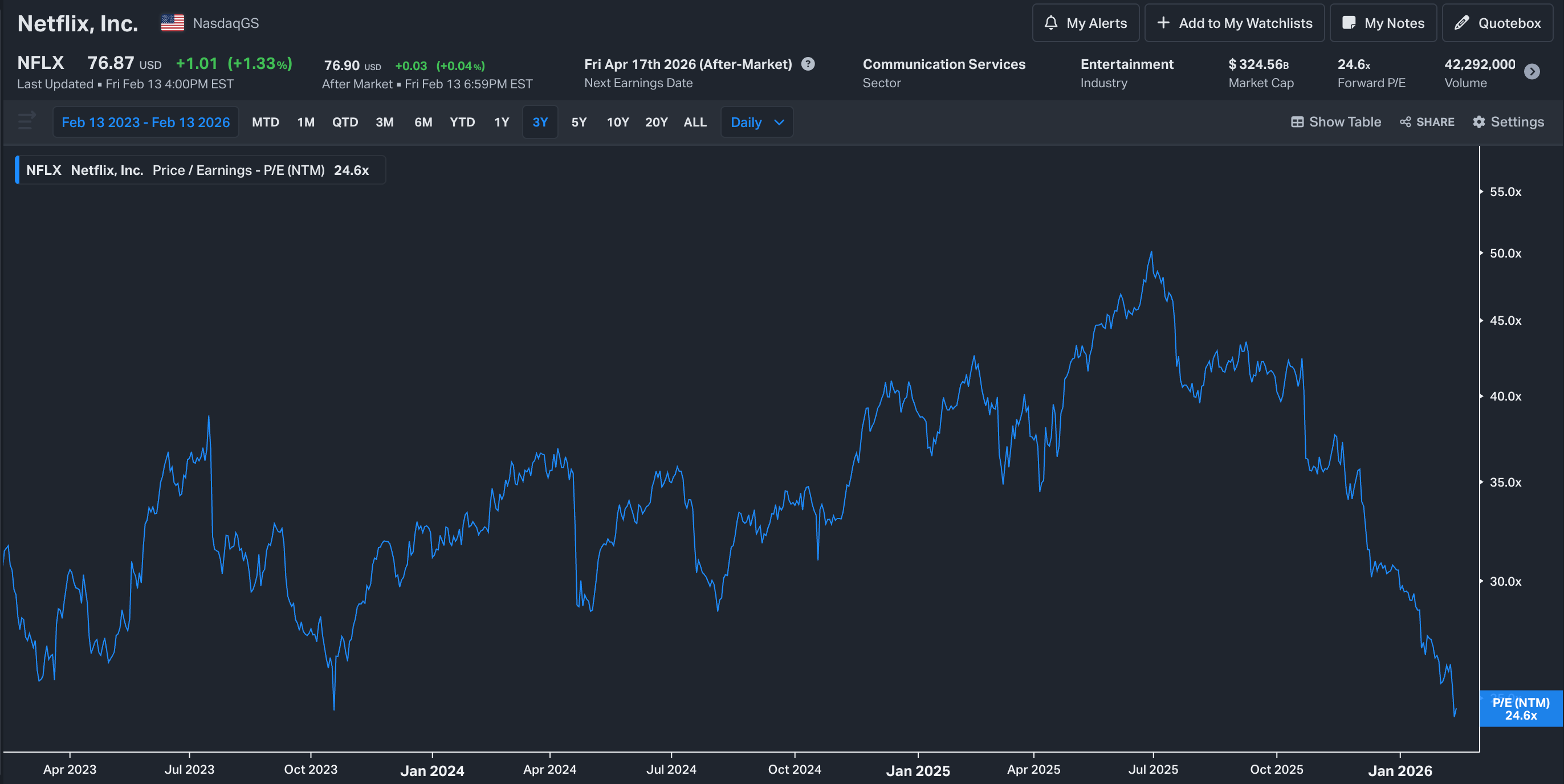

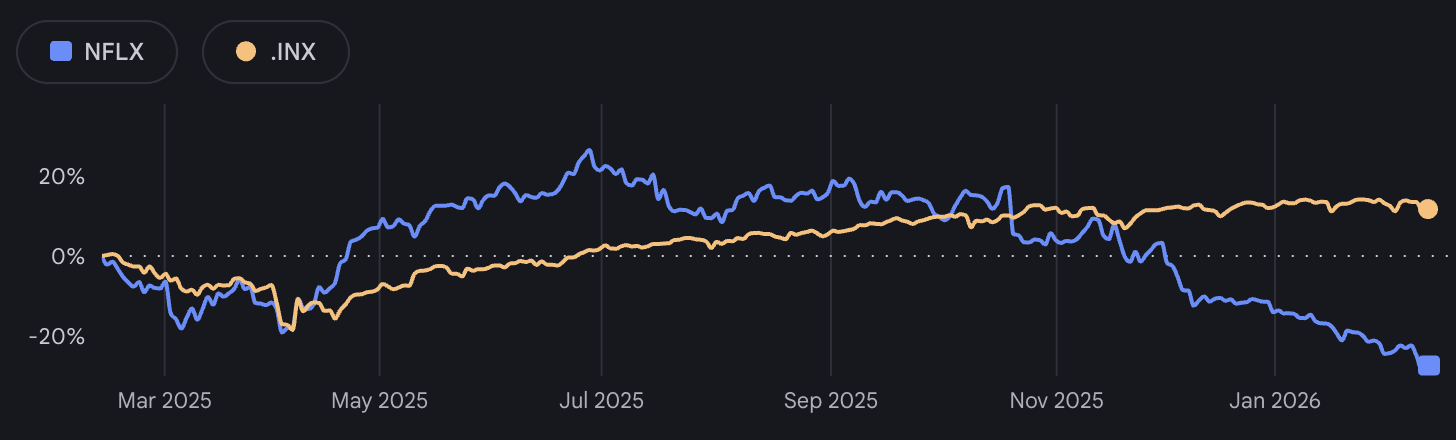

NFLX 0.00%↑ has sold off quite a bit, down over 40% from its 52wk high of $134.12. It’s now trading at a 3 year low PE ratio of 24x NTM earnings. I think the reason for the sell off is primarily concern over the acquisition of WBD 0.00%↑ and the uncertainty regarding that. You can see that NFLX 0.00%↑ diverges from the broader market in early December of 2025, right when the acquisition was announced.

I think this fear is pretty overblown, as even if the deal does fall through, Netflix has shown that they understand how to lower churn and maintain subscribers, as they have ramped up the number of event-like showings over the past 12-18 months.

Since January 2025, Netflix has a WWE Residency, airing WWE Raw live every Monday night. Netflix has partnered with the NFL to air games exclusively, as well as the MLB, where they will cover opening night this coming March. They also broadcasted Alex Honnold free climbing Taipei 101 in Taiwan just a few weeks ago. I think Netflix will continue this trend, so that they have more sports/YouTube-like content on platform, and attract viewers of that style of content.

If the deal goes through, I don’t see how Netflix doesn’t immediately re-rate upwards to ~30x NTM PE. This alone would drive returns of about 20%, not taking into consideration the new subscriber base acquired via WBD.

Positives

Substantial user-base regardless of acquisition fall through.

Increased events and integration of sports

Lowering movie theater exclusivity periods

Negatives

Regulatory concern with WBD 0.00%↑ acquistion

Platforms like YouTube/Twitch/Instagram Reels eat into watchtime for younger generations — meaning there is less of an appetite for longer form content on Netflix. If the trend of younger generations being less into TV shows/movies continues, this could be a long term risk for companies like Netflix and Disney.

What would an extreme bear case look like?

As part of my back of the envelope math, I failed to show what the downside would be if the deal fell through entirely, so I thought I’d add this section.

In this extreme bear case, share price falls from $76.87 to $51.57, a 32.91% loss. This is driven by no subscriber growth, acquisition not going through, and average revenue per user staying flat. I think the likelihood of this scenario is exceedingly low, but I thought it could be worthwhile just to show what that might look like.

The Trade:

I personally think that Netflix is a quality company that will continue to grow in subscriber count over time, and that this WBD 0.00%↑ acquisition is just a way for them to speed up that process while gaining content and IP that will increase customer retention over time. Their continued development and iteration of event-style content will enable them to compete with the likes of ESPN, YouTube, and Twitch in the years to come.