META: Social Media's Big Tobacco Moment?

3/27/26

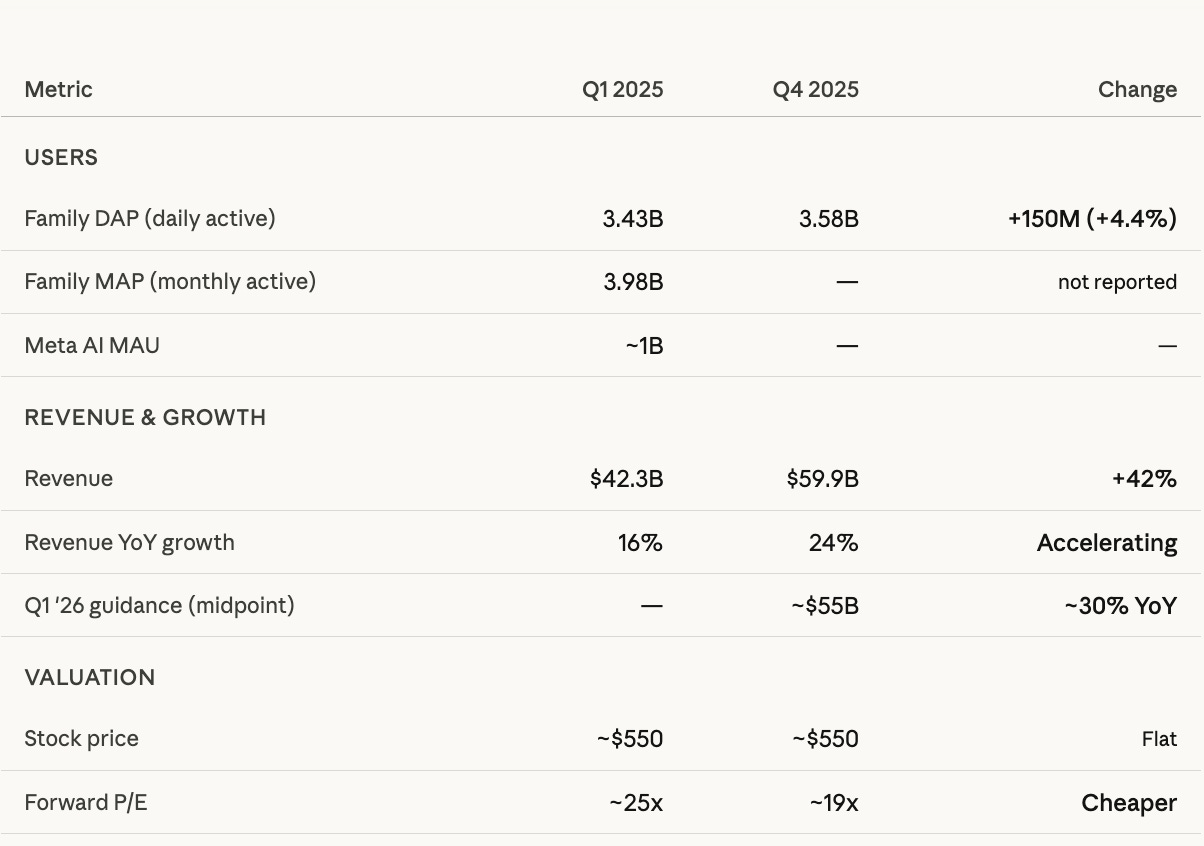

$META is back below $550 ($525 at the time of writing this) for the first time since the April tariff scares of last year — despite significant financial improvement since then:

Obviously there have been significant macro developments in the time since April of last year, namely the ongoing conflict with Iran that remains to be a murky situation.

Meta’s Legal Concerns

The main reason that META 0.00%↑ has sold off so significantly is because of legal developments surrounding the mental impact on the younger users of their apps.(Reuters)

The prevalent bear case is that this is just the beginning and that there are 3000 similar cases looming in the California court system, let alone more globally. It’s also been posed as social media’s “Big Tobacco Moment.”

What I find to be the interesting question here is what the outcome of these court cases will be to the end product of Meta, attention. I think that while these cases, and the precedent set by the most recent case can obviously cost Meta billions in legal fees, the bigger question is how will all of this change Meta’s core business structure.

Will Meta be forced to make their platforms less addictive? Removing the endless scroll, curated feeds, and targeted advertising would certainly harm their business.

But if the age gate is moved up (currently 13yo in the US) to 16 or 18 years old, I don’t see this having a significant impact on their business for a few reasons.

Teens will find a way around age gates. As someone who grew up with video games, social media platforms, etc. it is easy to just lie about your age or sign up in your parents name.

I would expect that teenagers have far less disposable income, and therefore advertising to them, while valuable, is not that substantial of an income source compared to adults and seniors.

Teens have had social media for years now. A 13 year old today was born in 2013. They experienced the covid lockdown at 7 years old and are likely daily users of Instagram, YouTube, etc. If the age gate moves up to 16yo or 18yo, they will simply find ways around it, or just wait a few years and be back on social media as if nothing happened.

If the incoming regulation is a more structural change to their apps like what I mentioned previously (removal of the endless scroll, curated feeds, and targeted advertising) then I think this $150b+ market cap sell off is warranted to some extent.

However, I find this extremely unlikely. The endless scroll, curated feeds, and targeted ads have been the norm of social media since late 2019-early 2020. This level of sweeping regulation would have massive implications. Is it possible, sure, but far from likely.

What I find to be more likely is that META continues to sell off as the litigation continues and that this narrative is similar to Google’s antitrust concerns in 2023. Meta and Google will likely have to pay billions in legal fees, but this seems more like a short term headwind than a structural risk to their business.

Meta’s AI Spend Concerns

Another portion of the META sell off is likely due to their increased AI spending, as anyone who has followed Meta for some time now, the market is typically not a fan of Zuckerberg’s capex tendencies.

Meta joined other mag-7 companies in 2026, projecting massive capital expenditures on AI of $115-135b in FY26. This announcement was made in the Q4 2025 earnings report on January 28, 2026, and the stock is down ~30% since.

Meta is not alone in this sell off, as many of the mag seven stocks are down as well, but part of the reason why I think the sentiment/narrative surrounding Meta’s capex is so negative is because Zuck has shown a propensity to keep investing even when the market is telling him to stop. (see Reality Labs spending in 2021-2022.)

The flip side is that Zuck has also shown an inclination to allocate capital to shareholders via buybacks and dividends when the stock remains lower than historical levels.

Zuck has also shown a willingness to make the company leaner, with sweeping layoffs in recent years. Additionally, in the 2022 sell-off, Meta bought back roughly 168 million shares, roughly 6% of the outstanding shares. So, if we see an extended drawdown to lower multiples, (we’re already at ~17.7x FWD PE) I believe that they would get aggressive with buybacks again.

Meta’s Recent Stock Based Compensation Plan

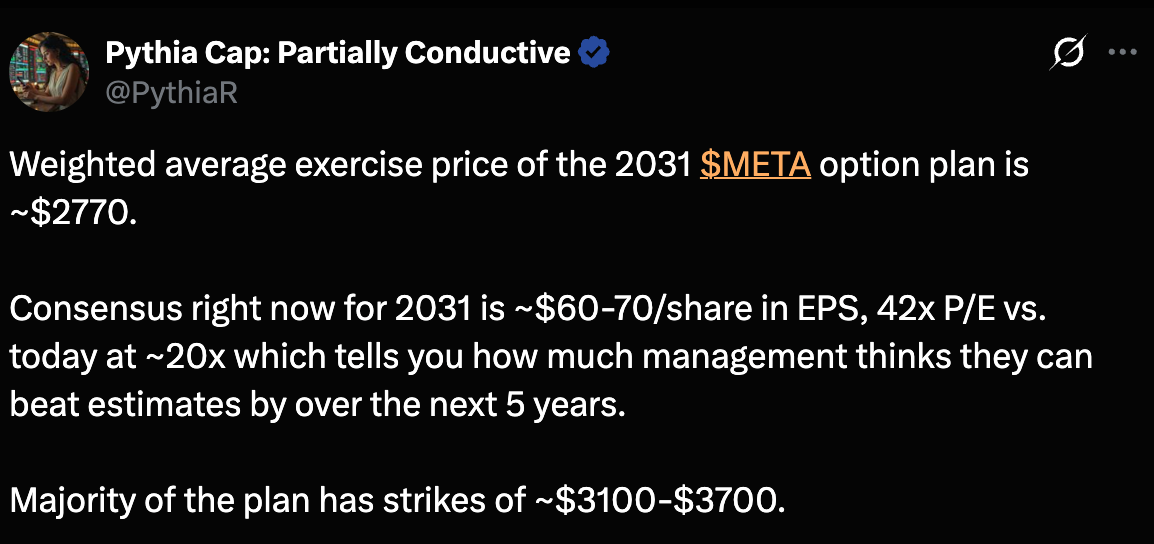

Another key headline that got lost in the recent volatility is the SBC plan that Meta recently announced. It’s interesting to discuss because while it looked overly aggressive when it was announced, it looks even crazier after the company has dropped ~$150b in market cap.

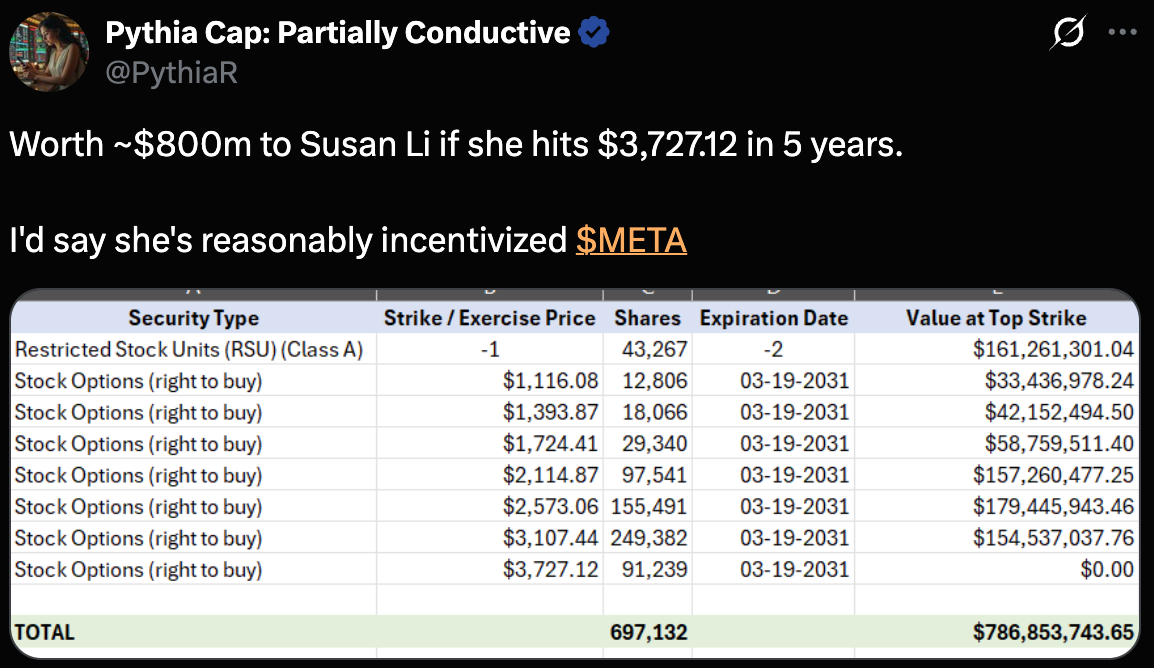

The option plan’s strikes are extremely high, ~$2770 on average, which implies a 31% CAGR from current levels shows internal confidence on levels I haven’t seen before. Additionally, Meta’s CFO, Susan Li, is strongly incentivized to drive even more extreme returns for the company:

While a $7 trillion market cap seems hard to believe, the incentives are there, and you could have said a similar thing about NVDA going from $745 billion in ‘21 to $4.1 trillion today. Obviously it gets harder as the numbers get bigger, but I find it hard to be pessimistic about a company that dominates the social media space, and has ~1/2 of the world as part of its DAU base.

If management is this confident internally, the market's pessimism may be overdone.

Trade Recommendation and Position Sizing

What I learned from my first go-around with META 0.00%↑ in 2022 is that the market can move against you far longer than you think it would. While I acquired ~100 shares for around $170-$180/share, and did very well on that investment, had I been more patient with my investment, I could have added to Meta sub $100, which I deeply regret missing out on.

With that being said, we don’t know if this will last nearly as long as the Reality Labs sell off. This could be a short blip in time where Meta falls ~30-35% off all time highs and recovers after the macro situation clears up. Or we could be in for a 50% drawdown and further war escalations could drive the whole market down.

That’s a long way of saying I have no clue how low Meta will go. The chart guys on Twitter seem to be confident it’s going to ~$475 or roughly another 10% lower from these levels. I have no expertise with charting, so I defer to their judgment, but I think that I’m going to start investing at these levels.

In terms of vehicle for this trade, I think shares are the only logical choice right now. The market seems to be far too volatile for LEAPS right now, and if you buy an ATM leap and META goes down even just 10%, your position is likely down close to 30% or more.

You can look at cash secured puts, and I have been, but you really have to tie a lot of capital up ~$50k per CSP, but the premiums are there. If you sell a January 2027 CSP, at $530/share, you get $7,200 in premium or roughly 13.5% on your money in that time period. If you get assigned, your effective cost/share is ~$458, which is not too bad, but obviously you tie up a lot of flexibility if the market continues to move against Meta.

Personally I will continue to buy shares as Meta goes down, but if there’s a significant narrative shift, and some of the legal headwinds subside, I will consider LEAPS, as I think Meta is positioned really well amongst its peers in terms of growth prospects vs. current valuation multiple. Currently, I would start with 1/4 of what a full position looks like, and have cash ready to deploy if Meta continues to fall.

If you enjoyed this writeup, consider subscribing, as it’s totally free and helps me out a ton. I post about stocks, prediction markets, and finance in general.

Disclaimer: This is not financial advice, do your own due diligence please.