Meta is a $1000 Stock

Why the world's best advertising business is still mispriced at 18x forward earnings

Finance teaches you that there’s no alpha in large caps. That everything is priced in. In my years of investing I’ve mostly adhered to this, trying to be unique with how I find and pick stocks.

But for some reason, there remains alpha within one of the largest companies in the world, and it seems to be available on a regular basis. I’m talking about Meta, which for some time now has traded as an AI loser, despite showing enormous returns, expecting massive forward earnings growth, and maintaining a reasonable valuation.

Why is this Opportunity Available?

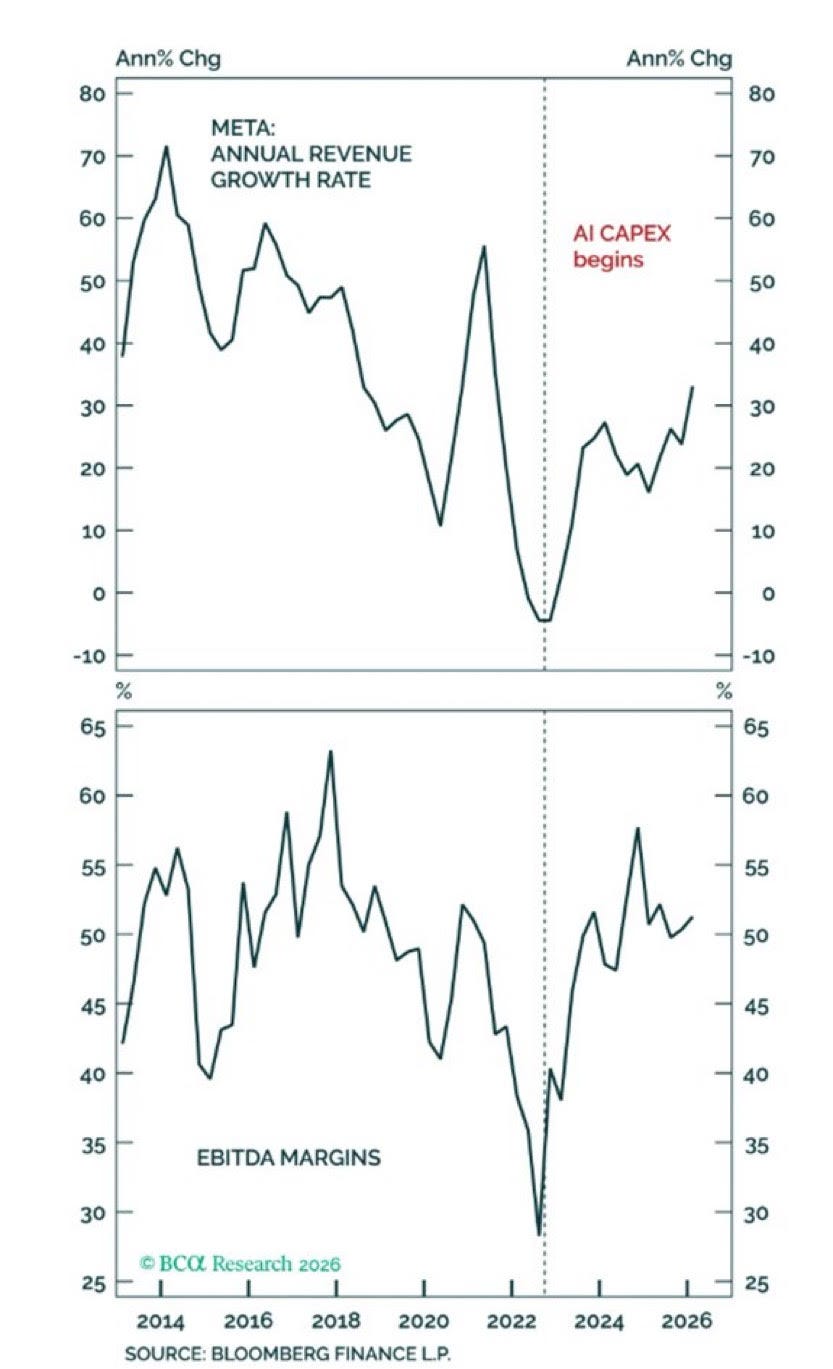

With every capex increase over the past few years, Meta stock has traded down. People seem to have PTSD from the Metaverse/VR spending cycles of ‘22. The datacenter capex is substantially different for multiple reasons which I will get into here.

Firstly, datacenters take ~2 yrs to get online, and Meta spent $28b in DC-related capex in 2023, so we are starting to see the first signs of AI-improved ad impressions + pricing. Anecdotally as well, Instagram’s Reels algorithm is by far the best at keeping my attention, as well as others. It is not uncommon that I will open Instagram to find 5+ reels from some friends.

Additionally, their ads are by far the best of any social media platform. X’s video ads are pure slop, and the text posts are completely nonsensical. YouTube’s advertising is pretty good, but I have only ever bought something from an ad on Instagram personally.

Secondly in regards to the AI spend, xAI (and neoclouds) have recently shown that there are multiple paths to monetizing compute, with Zuckerberg himself saying this in Q3 of 2025:

Like almost every week, people come to us from outside the company asking us to stand up an API service or asking if we have different compute that they could get from us. And we haven’t done that yet, but obviously if you got to a point where you overbuilt, you could have that as an option.”

Thirdly, they have massive distribution channels with 3B MAUs on Instagram, and even more across WhatsApp and Facebook. If models are going to be commoditized, and largely homogenous across companies, than distribution channels to customers is going to be a major differentiator.

The Increasing Diversification of Meta’s Business

Google has grown to become such a large company mostly on the back of their core business, but also their “other bets” that have grown into massive divisions. I believe Meta is in the early innings of their own version of “other bets” and I see clear paths to each of these being substantial divisions in their own right.

Developing their own OpenClaw with MuseSpark

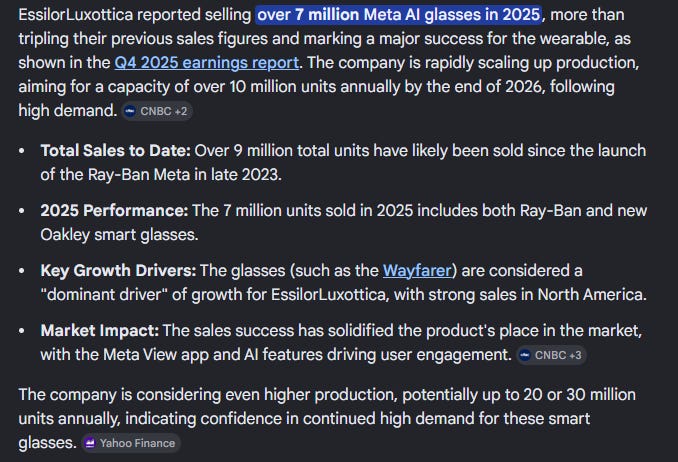

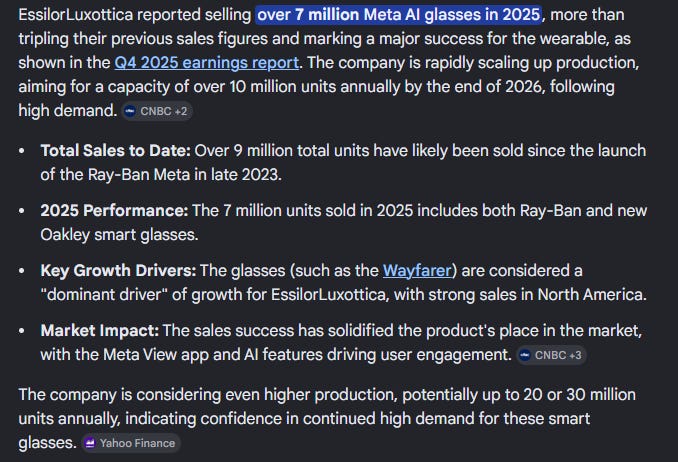

Meta Raybans - AI infused glasses

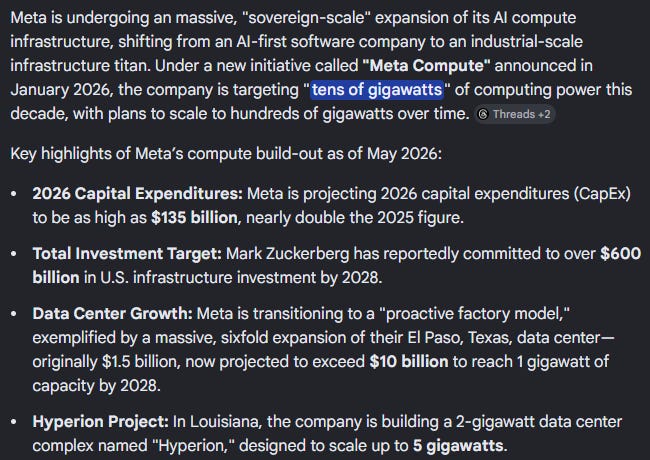

Massive amounts of compute for the exponentially increasing demand

VR, AR, Meta AI assistant

So What?

It’s my belief that Meta presents a similar opportunity to Google in early 2025. It’s a company that everyone knows, understands, yet they are missing the forest for the trees. Yes, Zuck is dumping boatloads of money into compute - but it’s already seeing returns. And guess what, if they end up not having a good use for the multiple GWs they plan to bring online, I’m sure Anthropic and OpenAI would be very interested.

For some reason, you can get one of the best advertising businesses in the world for 18x forward EPS. Also it’s growing revenues at 30%/yr. Oh, and they’ve also shown a willingness to buyback shares and get lean when the stock price tumbles. I think once Meta’s products, or AI-related returns meaningfully show up in the numbers, they are due for their own ‘Gemini 3 Moment’ like Google had last November.

In my opinion, once this happens they are very clearly a 30x PE company, with consensus EPS estimates around $35 for 2027, this quickly turns from a $600 stock into a $1000+ stock as soon as next year. Obviously to cause this re-rating, there would likely be a substantial EPS beat, so the stock could well exceed $1000.

The funny part about this is that for Meta, and for the S&P as a whole, 30x earnings has been pretty reasonable. Their average PE ratio since IPO is 29.4x, and the S&P’s current forward PE ratio is 20.9x. Meta is trading like a peer amongst the S&P despite its exceptional results, and I believe this is a temporary mispricing similar to the drawdown in ‘22.

I am personally long Meta, and increasing my position such that it is my largest by far.

Disclaimer: This is not financial advice, do your own due diligence please.