Hyperscalers vs. Semiconductors. Where Do We Go From Here?

7/8/2026

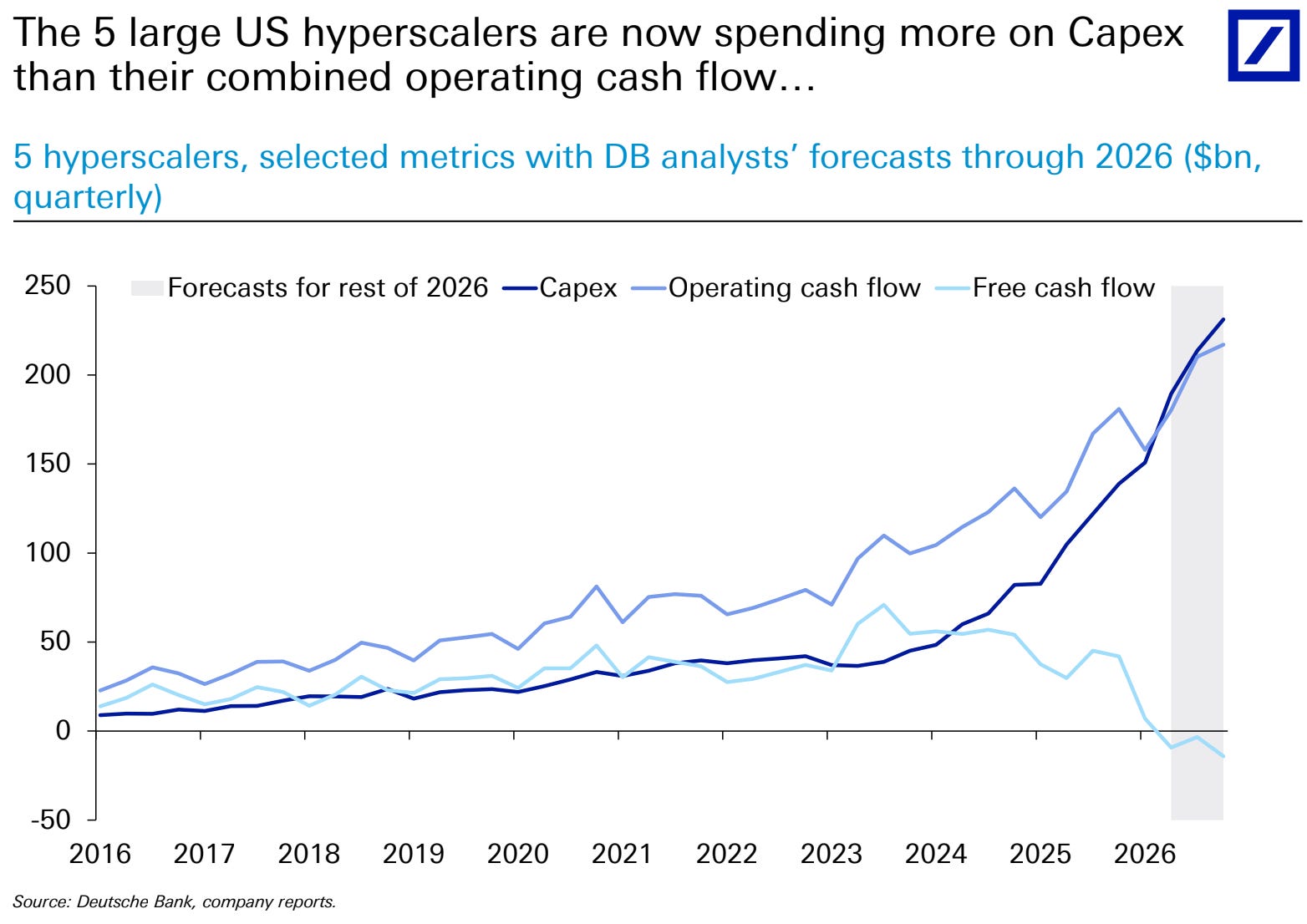

If you’ve followed markets recently, the overarching story has been that hyperscalers are being taken to the cleaners by the memory companies, with capex ballooning to record levels.

This is not projected to stop, as these companies, for the time being, are adamant about continuing to acquire compute at high costs. The problem? The market wants to see clearer returns on investment.

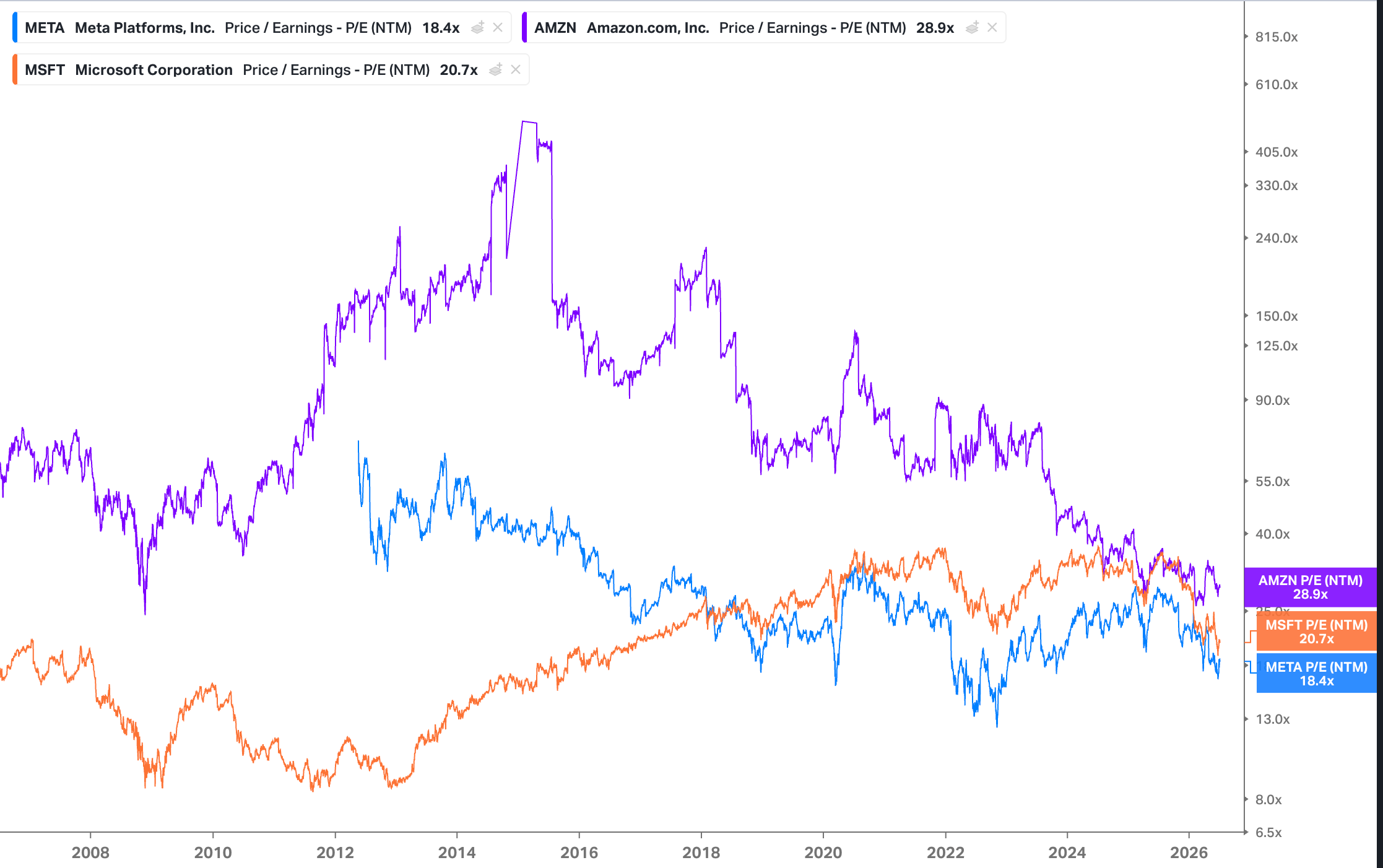

Taking a look at the valuations for these hyperscalers, you can see they’ve taken a hit from their historical levels. Specifically, the group of AMZN, MSFT, and META have taken the largest hits, which you can see in the next graph. Apple, despite facing increasing memory costs in all of their hardware, is helped by the fact that it has not made significant capital expenditures in this AI spending wave.

What’s the Point?

Up until this point, this article has been mostly descriptive, and not predictive of what I think will happen. I wanted to provide an unbiased overview of the current state of the market before getting into my beliefs about these companies.

With that being said, I have a few key beliefs about the current state of things.

These semiconductor valuations, as well as market sentiment do not make sense. To explain, let’s look at those capex projections again.

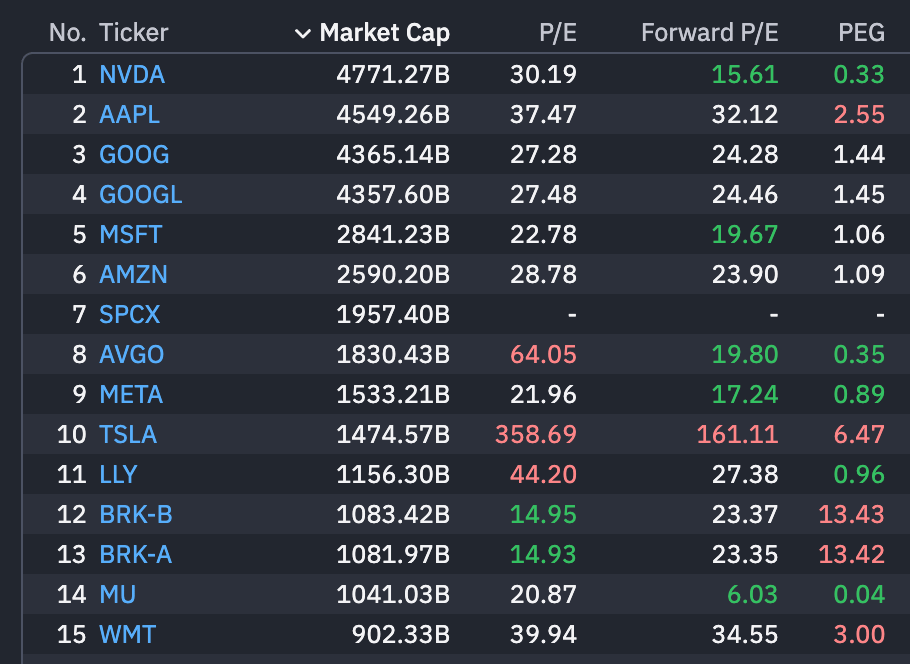

BofA’s latest report has capex for GOOGL, META, and AWS at over $1.5 trillion for the next 2 years, not including 2026 spend. That does not include MSFT. Yet, NVDA, which you could logically presume to be a major winner from this level of capital spending trades at 15x FWD earnings. Alongside that, the memory companies which have gone parabolic over the past year, still trade at single digit PE ratios.

The only way that those valuation levels make sense is that these capex projections are totally off, there is some silver bullet coming for memory utilization in LLMs, or that somehow the capital decision making of these 85-90% margin memory companies will erase the massive returns they are earning now. I find those unlikely.At the same time, there is this belief within the market that hyperscalers are willingly overspending, and that there is no line of sight to ROIC on this massive capex. I'm against that idea for a simple reason: these companies have highly intelligent founders and capital allocators at the helm.

They have a vested interest to make high returns on their capital decisions, and have huge financial outcomes tied to making that happen. The idea that they would willingly misallocate billions of dollars is insane to me.In META's case specifically, I think the Metaverse pivot soured investors and gave Zuckerberg a reputation for lighting capital on fire. That's exactly why the setup is compelling, as if and when they show clear returns on this spend, the sentiment shift and re-rate could be violent, similar to Google’s sentiment shift in mid-late 2025.

Additionally, these companies have multiple paths to gaining ROIC on this capex: selling compute to frontier labs, running their own models, running other models locally, replacing large swaths of the workforce via the improved productivity of AI-enabled employees, along with others.The market is pricing the outcome of AI as zero-sum. It feels as though there are no days where the hyperscaler/Mag 7 factor can be up while the semis factor is up.

The sentiment is that semis spend is unsustainable and that the hyperscalers are going to stop cutting checks and these semiconductor stocks will plummet. There is no middle ground or belief that this demand for semiconductor stocks could be a secular shift and not us spending at cyclical peak levels.

While I do not predict that we will spend trillions of dollars on datacenter buildout in perpetuity, I do believe there is some middle ground where the demand for compute grows at a high rate, while big spenders see a ROIC.

Actionable Takeaways

I believe there are a few key takeaways from this discussion. Firstly, if you are in the camp that we are at the peak of a massive overspend on compute, these hyperscalers can still be good investments. Many of these companies, namely Meta and Amazon, would re-rate massively if there were signals of capital discipline. It’s not as though their spending has impaired their core businesses, and while losses of hundreds of billions of dollars in the worst case would obviously hurt, these companies could earn that in operating cash flow within a few years.

Second, if you are a believer in this middle ground, NVDA at 15x forward earnings seems pretty attractive. Not to mention the memory companies that are printing cash right now. Samsung just overtook Nvidia as the most profitable company in the world, with ~$58.5 billion in operating profit for Q2 2026.

Lastly, I want to emphasize that I was not a market participant during the 2000s dot com bubble, and I have seen many claim that those who lost money were foolish or were making terrible investments. When we look back at financial crises, we see the real figures, the real EPS that happened, and not the forward earnings projections made by the market. In hindsight, it is always easy to call something overvalued or investors stupid for thinking pets(dot)com was a good investment.

The reality is that I’m sure a lot of sound, rational market participants lost money in 2000, and that things probably looked logical in a forward valuation sense. While I am not an AI bear, I do see possibilities for this shaping to be another situation similar to that, and for that reason I have shifted many of my investments to these mag-7 companies which have the benefit of having sustainable core businesses that are positively affected by AI.

I think one of the key things to watch is how concentrated the compute becomes. As SpaceX, and potentially Meta sell their “excess compute” to Anthropic, the “key man” risk increases, and the demand for compute becomes reliant on few companies.

It is also important to note that many of the current subscription models do not seem to be sustainable for Anthropic/OpenAI, as they continue to try to shift certain models to token-based billing, despite the consumers distaste for that model. The level of subsidization of these models remains a key discussion point for bears and bulls, but without internal company data it is pointless to argue over.

My hope is that these companies IPO sooner rather than later, so that we can have line of sight into these factors, but it seems the SpaceX IPO, Google equity raise along with the coming SK Hynix ADR, may be sucking the air out of the room for some time.