Commodity Futures Are Simple, Actually

11/10/25

Last Fall, I sat down in my Derivatives class fully expecting to feel like I did in AP Calculus back in high school. In over my head, totally confused, etc.

In reality, I had one of the best teachers of my college experience (from Goldman Sachs) and was able to fully comprehend what I believed to be complex financial derivatives with ease. I got 100% on every exam and the class was the highlight of an otherwise mundane semester.

Since then, I haven’t been able to really use that knowledge in any of my pursuits, academic or otherwise and I regret that. I already felt as though I was losing some of the knowledge that I worked hard to understand.

I am of the belief that most concepts are like languages. If you don’t use it, you’ll lose it, and I don’t want to lose this knowledge. It also makes you seem smart if you can bring up complex financial derivatives.

In the effort of not losing this knowledge, I thought it would be a good idea to explain the basics of derivatives in written format here. So, let’s start with futures.

The T-Shirt Business Example

Imagine you are a t- shirt manufacturer. Your costs are mostly fixed in terms of labor and manufacturing overhead, but they are highly sensitive to the price of cotton moving up and down. This is a problem. How do you price your products if you are constantly at a risk of one of your main costs increasing?

What if you could lock in a price that you are willing to pay in the future to make sure that the numbers work for your profits? Well you can. That’s exactly what futures allow you to do.

The Mechanics of Futures

Futures are contracts to buy or sell a specific asset at a predetermined price in the future.

This language is very specific because futures are standardized, as opposed to forwards, which deal with currencies.

Futures are most commonly associated with commodities, but you can trade futures on indexes as well.

Futures are traded on 40 different exchanges, the largest being the CME.(Chicago Mercantile Exchange)

Every futures contract has specs: the most important being the size or amount of the asset being traded, and the quotation or how it is quoted on the exchange.

For example, the size of a wheat contract is 5,000 bushels or roughly 136 metric tons, and Wheat is quoted in US cents per bushel on the CME.

This is important to understand the scale of what is being traded and to keep everything consistent.

The Four Main Users (and Uses) of Futures

The next concept to understand is who is buying and selling these futures?

There are 4 main market participants that would buy and sell these futures:

Speculators: these are people who are quickly buying and selling these futures, thinking a piece of news or market narrative will drive commodity prices in whichever direction they’re betting on (think WSB degens)

Investors: These are people who also have a directional belief on a commodity, but their time horizon is usually much longer than speculators (think months or even years)

Hedgers: Market participants whose real life business has risks pertaining to that given commodity (think a t shirt manufacturer with cotton futures)

Arbitrageurs: This is your Goldman Sachs or Morgan Stanley trading division. They notice some sort of opportunity where there’s a large gap between SPOT prices and future prices

Now it’s also important to understand each of these participants risk profile and time horizon

From least to most risky they’d be ranked

Arbitrageur (obviously)

Hedger

Investor

Speculator

In terms of time horizon from shortest to longest, they’d be ranked:

Arbitrageur

Speculator

Investor

Hedger

The hedger has the longest time horizon because they are typically indefinitely exposed to some sort of risk. For example, the T-shirt manufacturer will have a risk of cotton prices increasing as long they are in business.

How Do We Price Futures?

The next concept to understand is how do we price futures? If 5000 troy oz of silver is worth $250,000 today, how much should it be worth in 1 year?

To understand what something is worth in the future, we have to think about the costs associated with holding it, as well as the benefits of holding it. This is referred to as the carrying cost model.

For a commodity like silver, there are storage costs of holding it, you have to think about security and keeping it indoors away from the elements, but there aren’t many benefits to holding silver unless you have a corporation that can use it.

For a commodity like crude oil, it still has storage costs, but it has many more benefits of holding it and is much more useful than a commodity like silver.

To price futures, you have to add the costs of holding them and subtract the benefits of having that physical commodity. That sounds counterintuitive, but it makes sense if you think about it.

You add the costs, because you would be incurring those costs to hold that asset. You subtract the benefits, because you would also be reaping those benefits if you held the asset.

Those benefits of holding that asset vs. the future is called a “convenience yield”

The convenience yield is a premium associated with owning the physical commodity and it is high when supply is tight.

So how do we calculate the convenience yield?

Well we can use the cost of carry model where:

Futures Price = Spot Price x (1 + Carrying Costs - Convenience Yield)^Time

Let’s look at crude oil with this model

SPOT WTI Crude is at: $60.89/barrel

1 Year Futures are at: $59.57/barrel

Assume storage costs = 4%

1 yr risk free rate = 3.75%

59.57 = 60.89 x (1+0.0375+0.04 - Convenience Yield)^1

In this example, the costs of holding oil are 7.5%, and the Convenience Yield works roughly out to 10%. So, it is more valuable to have oil physically than hold the future contract.

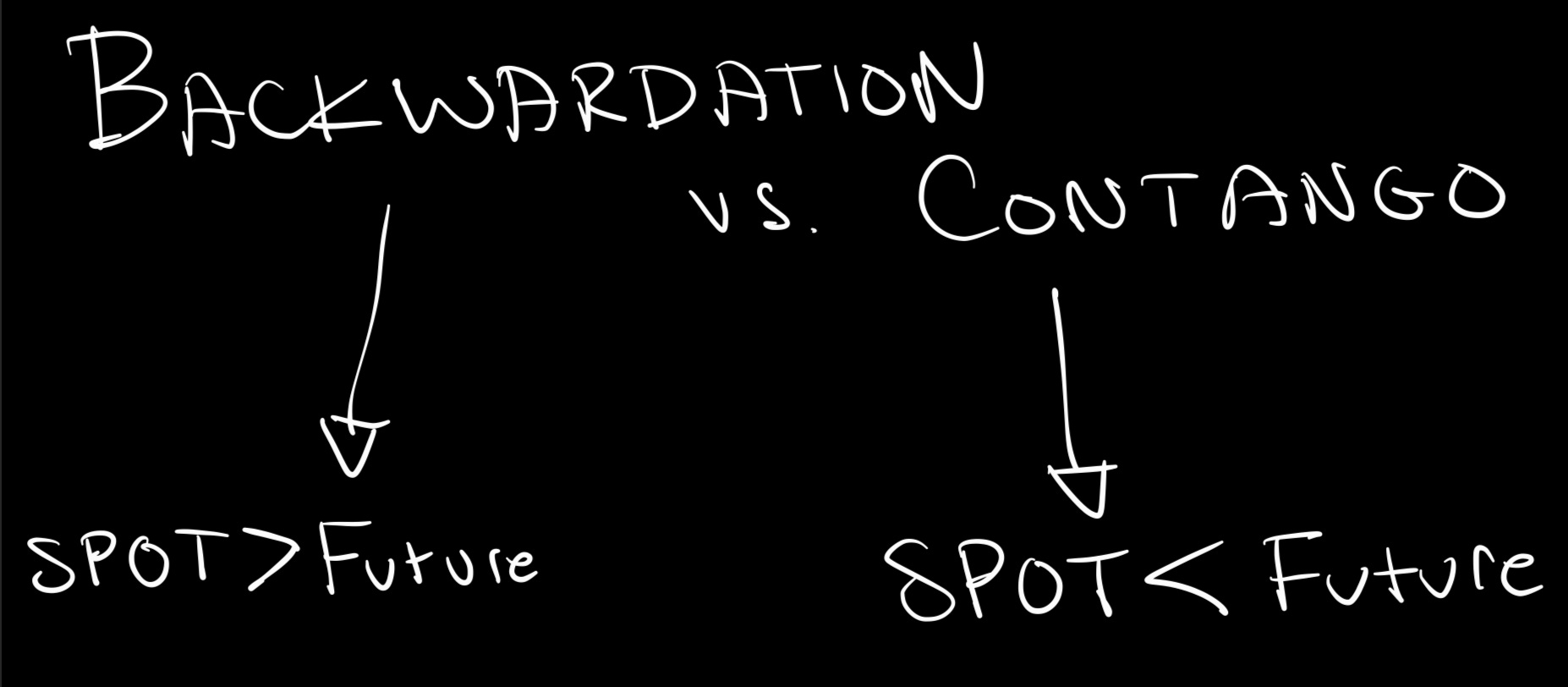

This phenomenon is called BACKWARDATION, and it occurs when near term demand is higher than we expect future demand to be. But honestly the prices are so close that this is like saying you are underwater after dipping your toe in the pool. If the future price was trading at $40/barrel, then there would be a real story here.

The inverse of this situation, and where most commodities trade in normal times is called CONTANGO. This is when SPOT (or current) prices are lower than future prices. This is the normal state because it takes into account carrying costs like storage, insurance, and interest rates.

Close, Roll, or Deliver (or Receive)

There are three things you can do with a futures position:

Close: Buy or Sell to close your position

Roll: Close your position while simultaneously opening another similar position (likely the case if you are a hedger)

Deliver/Receive: Depending on whether or not you bought or sold a future, you can receive or deliver the asset (this is the most uncommon by far)

The Power of Futures (and Derivatives)

Why would you want to use futures? Well they (and all derivatives for that matter) offer this beautiful thing called leverage.

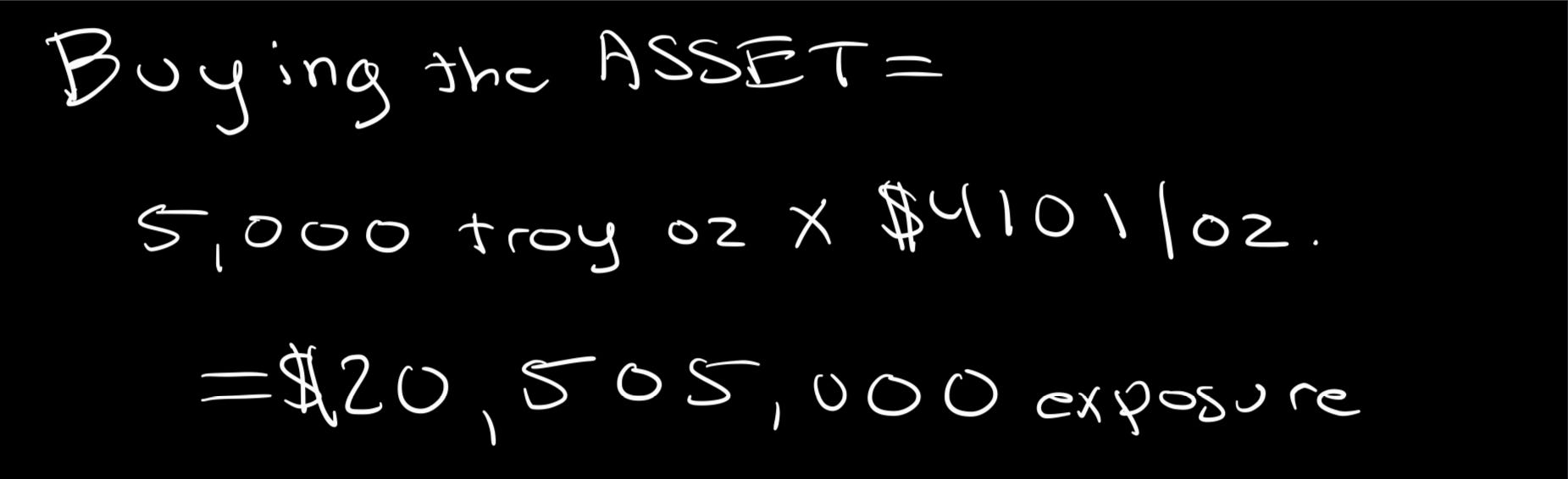

Let’s say you wanted exposure to gold as a portfolio manager with $200mm AUM.

The first way you could get exposure is buying the physical asset. The math would work out something like this:

This is not taking into account that you’d have to store the asset or any of those concerns. It would cost you $20.5 million to get roughly 10% in exposure to gold.

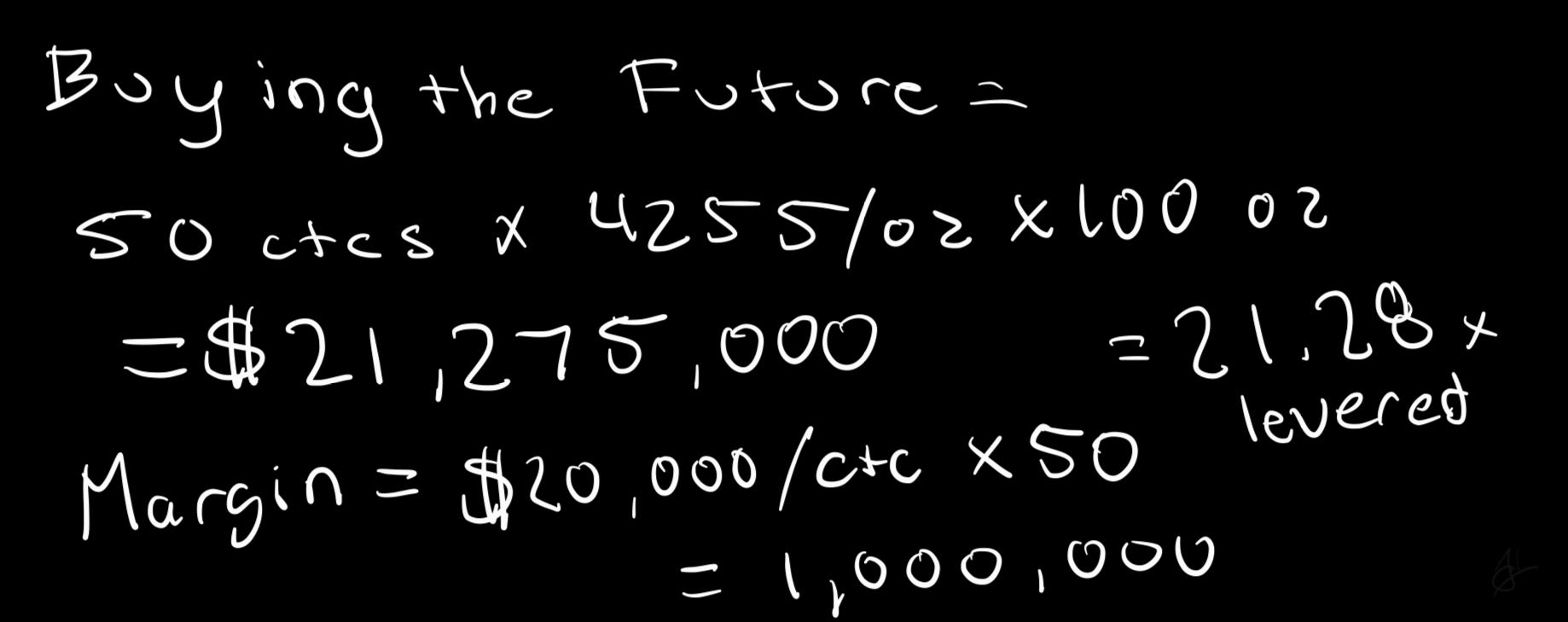

Now let’s say you wanted exposure to gold but didn’t want to tie as much capital up in that trade:

In this scenario, you’re spending $1,000,000 in margin (collateral you post to hold the position) for a position that moves like one worth $21,275,000. Margin is a bit more complicated than that, but that’s the basic idea.

This gives you 21.8x leverage and let’s you use $19 million elsewhere.

This leverage is something that all derivatives facilitate and obviously comes with its own risks, but does make for exceptional returns if used correctly.

That’s pretty much the basics when it comes to understanding commodity futures. Futures arbitrage is pretty complicated and probably requires its own article, which I may write later.

Please consider subscribing if you’d like to read my future analysis of the stock and real estate markets, as well as the rise of prediction markets. In the future I plan to do more stock specific research on companies that interest me, as well as articles on what I believe companies are doing well or poorly and my recommendations for them.

In the meantime I have a catalog of stocks that I researched during my summer internship in 2024, which can be found here. I also summarized this research as well as some of my larger portfolio positions in this post.